The Penny Hoarder |

- 12 Best Personal Finance Podcasts to Make You Smarter About Money

- How to Cancel a Free Trial Before You Start Getting Charged

- Solid Marks for Gabi Insurance Review

- Buying These 9 Reusable Products Can Help Save Money Over Time

| 12 Best Personal Finance Podcasts to Make You Smarter About Money Posted: 14 Apr 2021 11:00 AM PDT Everyone wants to know these days: What are you listening to? We still love a good book recommendation and a deep-cut Netflix tip, but what we're all craving in 2021 is a podcast we can beam to our Airpods while we power-walk away our quarantine 15. While true-crime stories and celebrities discovering WFH life dominate much of the podcast scene, the beauty of the medium is the variety at your fingertips — nearly all of it absolutely free to consume. If you have money on your mind, there's a podcast to help, whether you want education or commiseration. 12 Best Personal Finance Podcasts in 2021Next time you're clipping your coupons and working on your budget, tune your ears to one of these personal finance podcasts. 1. Planet MoneyA perennial favorite, this long-running NPR segment and podcast Planet Money has a way of turning even the most complex or mind-numbing facets of economics into clear, often fun explanations about how money rules our world. It won't tell you how to budget or where to invest, but you can tune in for the short, 15- to 30-minute episodes twice a week to learn something that'll make you sound smarter at a cocktail party. 2. HerMoneyFinancial journalist and entrepreneur Jean Chatzky's half-hour interviews in HerMoney dig into money issues with women in mind but without the froufrou lady branding. Topics range from expert tips to discussions on the psychology of money, all with the philosophy that "women need financial advice specifically for them." 3. Bad With MoneyThrough interviews with experts and personalities, Bad With Money host Gaby Dunn answers some of our most personal and most pressing questions about money. Expect a lot of personality from the host, too, who is a journalist-actor-comedian. From paying for mental health care to for-profit prisons to student loans and investing, you'll find something to illuminate your relationship with money in this podcast, now in its seventh season. Episodes tend to hit the 45-minutes mark. 4. So Money With Farnoosh TorabiIn this thrice-weekly podcast, you'll get everything from interviews with entrepreneurs to personal stories of financial success to personalized money advice from a journalist, author and personal finance expert. In her popular So Money segment "Ask Farnoosh," host Farnoosh Torabi answers questions from listeners about nitty gritty topics like taxes, retirement accounts and investing. Episodes run 30 to 50 minutes nad focus on how your relationship with money can help you live a richer, happier life. 5. Motley Fool AnswersOne of a suite of podcasts from personal finance site The Motley Fool, Answers helps listeners make smart money moves. Hosts Alison Southwick and Robert Brokamp answer personal finance questions from listeners and break down timely money topics. Most episodes are focused on investing — including maximizing your retirement accounts — as that's the company's specialty. But you'll find plenty to learn about budgeting, saving, paying down debt and more. 6. The Clever Girl KnowsThe Clever Girl Finance site is on a mission to pay down debt, save money and build wealth. The Clever Girl Knows podcast is its companion for your ears. Host Bola Sokunbi, founder of Clever Girl Finance and a Certified Financial Education Instructor (CFEI), is dedicated to helping women take control of their finances. She cops to the money mistakes she made in her past, and she wants to help others like her overcome similar challenges and achieve financial wellness.   7. Frugal Friends PodcastHosts Jill Sirianni and Jen Smith (a former The Penny Hoarder writer) are the Frugal Friends. Through fun and accessible conversations and guest interviews, they share practical tips to help you spend less money. From meal planning to travel hacking, you'll find something to help you tighten your belt and still love life. Bonus: Every episode includes a listener-submitted "Bill of the Week," where the hosts and audience get to celebrate a listener's financial win. 8. Queer MoneyPartners David Auten and John Schneider, the personal finance bloggers behind Debt Free Guys, host Queer Money to help LGBTQ listeners live debt free, be money conscious and enjoy life. With expert guests, they cover money basics like what to do with your 401(k) when you change jobs, and intersectional topics like transgender health care and coming out at work. 9. Millennial MoneyCertified financial planner Shannah Compton Game talks about the nitty-gritty of setting yourself up for financial success. Millennial Money is instructive with a tough-love approach, mixing interview episodes with 20-minute monologues from Game. 10. Paychecks & BalancesHost Rich Jones promises to make conversations about work and money fun, relatable and informative. Paychecks & Balances calls itself "money with a millennial spin," but you don't have to be a '90s kid to find yourself nodding along with this show. 11. Brown AmbitionBrown Ambition is a weekly 60-minute show hosted by finance and business reporter Mandi Woodruff, and "The Budgetnista," Tiffany Aliche. The financial experts answer listeners' pressing money questions on career, success, building wealth and navigating money in relationships. 12. Afford AnythingHost and founder of Afford Anything Paula Pant interviews money experts, entrepreneurs and celebrities, and answers listener questions about money, business and financial independence. Weekly episodes run about 90 minutes. Dana Sitar (@danasitar) has been writing and editing since 2011, covering personal finance, careers and digital media. Lisa Rowan is a former writer for The Penny Hoarder. This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017. This posting includes an audio/video/photo media file: Download Now |

| How to Cancel a Free Trial Before You Start Getting Charged Posted: 14 Apr 2021 09:00 AM PDT Curious how YouTube TV works but aren't ready to sign up? Feel like binge-watching your favorite animated classics without forking over the $69.99 Disney+ annual subscription? Free trials can give you a sneak peek. But free trials aren't really meant to be free. The goal is to introduce you to a product or service and then hook you so you decide to keep it (and pay for it) beyond the trial period. Either that or the company is hoping you just forget to cancel so it can automatically start charging you. Ever wonder why you have to provide your credit card information to sign up for something that's free? That's why. If you don't want to become an unintentional paying customer, it's vital that you know how to cancel free trials. Consider the Cost Before Signing Up for a Free TrialSigning up for a free trial is a great way to test out a product or service without spending any money. But they can end up costing you if you're not careful. Even if you think you'll definitely cancel the service before your free trial is over, be cautious about signing up for something that doesn't fit into your budget. You don't want to fall in love with a service only to have no choice but to cancel it because you can't afford it. And you don't want to overdraft your account in the event that you don't end up canceling in time. In addition to hoping you don't cancel, companies also want to make sure they can actually get paid. Though a free trial shouldn't cost you anything, you may see a pending charge or pre-authorization on your account, which is basically the company's way of verifying that your account is legit. Avoid Paying for Subscriptions When Your Free Trials EndOne way to avoid going past a subscription's free trial period is to cancel right after signing up. You won't have to worry about remembering to do it at the end of the week or month or whenever the trial ends. However, it's important to note: Only do this if the company will continue providing the service through the end of the trial period. Some don't and will cut you off as soon as you submit your cancellation. Then you've wasted the opportunity to test out the service. Using a virtual credit card is another tactic to avoid paying for subscriptions past the trial period. Virtual credit cards are credit card numbers issued by some banks, credit card companies and independent financial companies. (You don't actually get a physical card.) These virtual cards often are restricted to a one-time use or have a short expiration period, which makes them favorable to people signing up for free trials. The startup DoNotPay has a similar service that generates virtual credit card numbers you can use for free trials. The card numbers can't be charged again after a trial period ends, and they aren't tied to your bank account. Then there's always the strategy of simply canceling your free trial right before it ends. Set a reminder (or two) to cut your ties with the service before payment becomes due. Most companies aren't going to send you a reminder that your free period is about to be over (though Mastercard requires some merchants to do so). Mark your calendar, set an alert on your phone or do whatever you need to remember to cancel. Pro Tip Regularly review your monthly bank statements or credit card statements so you can catch any unexpected charges — like a subscription you forgot to cancel. Make sure you read over the cancellation policy when you sign up for a free trial. Some companies require you to submit cancellation requests a day or two before the start of the first billing period. Generally, when you log into your account, there's an option to cancel under the section for billing or subscription management. There will probably be multiple prompts to convince you not to cancel, but don't let them sway you. How to Cancel 10 Popular Free Trial OffersWe browsed the cancellation policies of several popular services to get instructions on how to cancel their free trials. In every case, make sure you complete all the steps to confirm your cancellation. Lots of companies send email confirmations. These guidelines are based on canceling directly through each service. Canceling a trial you acquired through a third party — for example, a free HBO trial you signed up for through your cable provider — may require different steps. 1. How to Cancel an Adobe Free TrialHere are the steps to cancel a free trial of Adobe.

2. How to Cancel an Amazon Prime Free TrialAccording to the terms and conditions for Amazon Prime, you have three business days from when your free trial converts to a paid membership to get a full refund, provided you haven't used any of the Prime benefits during that three-day period. However, to cancel your trial before it switches to the paid version, visit this page and click the "End Membership" button. 3. How to Cancel an Ancestry Free TrialAccording to Ancestry Support, your free trial ends automatically once you cancel it, even if additional days were remaining in the trial period. Cancel Ancestry's free trial by following these steps.

4. How to Cancel an Audible Free TrialHere's how to cancel your free trial of Audible.

5. How to Cancel an Avast Internet Security Free TrialSee the steps below to cancel your free Avast trial before you get charged.

See here for additional instructions on how to cancel if you signed up using a different order distributor. 6. How to Cancel a Disney+ Free TrialAccording to the terms in its subscriber agreement, you can cancel at any time during your free trial and still enjoy the service through the end of that trial period. Follow these steps to cancel your free Disney+ trial from your web browser.

See here for more information about cancelling your subscription, including directions on how to cancel from some third-party platforms. 7. How to Cancel a Hulu Free TrialAccording to Hulu's terms and conditions, your service may end immediately upon cancellation. Follow these steps to cancel.

8. How to Cancel a Showtime Free TrialFollow these steps to cancel your free trial of Showtime via your web browser.

See here for information about how to cancel your subscription through third parties. 9. How to Cancel a Starz Free Trial

The "Cancel" tab on this page contains additional information about ending your Starz subscription from third-party providers. 10. How to Cancel a YouTube TV Free TrialCancel your YouTube free trial by following the steps below.

See here for additional information about cancelling on an Android or Apple device. Nicole Dow is a senior writer at The Penny Hoarder. This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017. This posting includes an audio/video/photo media file: Download Now |

| Solid Marks for Gabi Insurance Review Posted: 14 Apr 2021 09:00 AM PDT When it comes to my 401(k), daily alarm clock or, yes, even my rotisserie chicken, I've embraced the set-it-and-forget-it mantra. But for car insurance? You're doing yourself a disservice if you aren't shopping for better car insurance rates at least once a year. That's what makes tools like Gabi so helpful. In our Gabi insurance review, we'll weigh the pros and cons of using an insurance comparison tool, instead of directly working with insurance agents, when shopping for new car insurance rates. What Is Gabi Insurance?Gabi Insurance is a newcomer to the insurance scene. The San Francisco insurance company was founded in 2016, four years after The Zebra (another car insurance comparison site that I had mixed feelings about; get the full scoop in my Zebra car insurance review). While Gabi is known primarily for its auto insurance quotes, users can also rely on Gabi to compare insurance providers for renters insurance, home insurance, condo insurance, landlord insurance and umbrella insurance. (I could not find an option for life insurance.) Gabi is a fully licensed insurance broker in 50 states plus the District of Columbia, meaning they can underwrite, price and sell policies and handle claims. It also means that, when you generate quotes on the site, you can buy directly on the site. One of the issues with sites like The Zebra is that, after generating your auto insurance quote, you'd have to leave the site and go to the actual insurance company's site to complete the process. Gabi works with more than 40 top insurance agencies to help you find the best rate for your car(s), driving history and budget. Among those insurance companies are Nationwide, Travelers, Progressive, Clearcover and Safeco. Gabi claims it saves drivers an average of $961 per year and can provide quotes in a matter of minutes. It's time to test those promises. How Gabi Works: A ReviewGetting your Gabi insurance quotes can be relatively painless, depending on the route you take. You have three options:

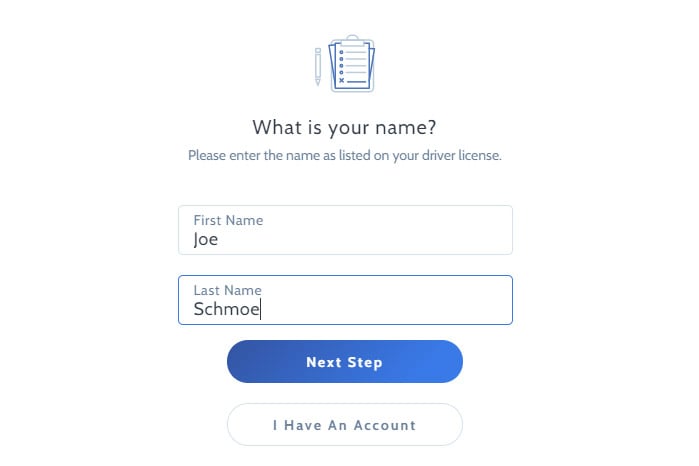

Because I'm private by nature (and because I just had the pleasure of dealing with a fraudulent unemployment claim in my name), I was hesitant to provide any login information. I first tried to advance without providing any information, but as we'll see, this doesn't get you very far. Eventually, I uploaded a PDF of my policy.  Getting started is easy. First you'll make your decision re: providing insurance information or not (more on that below). Then you'll enter your name. (Like I did when reviewing The Zebra, I started the process with the very real, honest name of Joe Schmoe.)  After providing your name, Gabi will ask for a handful of other contact info: birthday, address, whether you own or rent your home, email address and cell phone number. When asking for the email address, Gabi promises your information is never sold or shared. The Zebra says something similar, yet Geico conveniently sent an email to my inbox addressing me as Joe just minutes after I hit submit on The Zebra's site.  Contact update: As of two hours after creating my account, I have received one text and two emails from Gabi, but none from any third-party insurance providers. Could it be that Gabi is telling the truth when they say they won't share or sell your data? To Provide Insurance Info Or Not to Provide Insurance Info? That Is the QuestionThat's what Hamlet said, right? As I mentioned, in my first attempt at using Gabi's car insurance comparison platform, I resisted their pleas for my personal info. "They don't need to know anything about me to build a quote tailored to me," I foolishly asserted. But when I got to the magical part where Gabi was supposed to tell me I'm a schmuck who has been paying too much for auto insurance, I was instead given a list of common insurance companies, all with blue buttons that said "View My Quote." "Surely I must just click each and see a quote at the ready, despite the platform having no knowledge of my car, driving history or policy preferences," I told myself. Oh, Joe Schmoe, what a fool you are.  I quickly learned, upon clicking into Liberty Mutual, Allstate and Progressive, that giving Gabi such limited info meant the site would merely direct me to individual insurance companies to provide more detailed personal information to generate a quote. That's right: In that instance, Gabi serves no purpose, because you must start from scratch on every insurance company's site to compare. If you're unwilling to provide either your login info for your current insurance company or a PDF of your auto insurance policy, then Gabi is not right for you. In the name of research, I decided I was comfortable enough downloading a copy of my policy from Allstate and then uploading it into Gabi. While it does have some personal data within it, my email and password were still safe with me. It took only a few seconds for the artificial intelligence on Gabi's site to read my policy and tell me in intricate detail what those pages contained. (This is either really convenient for insurance shoppers or a warning sign that robots are just days away from taking over.) From there, I was able to input more personal information about myself as a driver, my partner (who is also on my policy) and our car. I tried to remove my partner for a good five minutes just for kicks and eventually gave up. Later on, I learned if I had just waited a few more clicks, I would have had the option of toggling secondary drivers on and off. If Gabi had made that clear, it would have saved me time and frustration. Actually generating my quotes did take about a minute, which is notably fast. However, I had just used The Zebra a few days before, and that experience was faster, so Gabi seemed slow by comparison. The Car Insurance Quotes I Got from GabiI was pleasantly surprised to see a few insurance agencies whose names I recognized among my top results. And the savings were quite large.  My top quote came from Stillwater and would save me $622 a year. I was dubious upon seeing that, so I clicked into the "View Details" portion of the quote and did find some discrepancies. The largest: My property damage coverage dropped from $500,000 with my current policy to $100,000 with this potential new policy. Still, the changes were so minor that it ultimately felt like a good deal. But buyer beware: You shouldn't necessarily expect your current policy and quoted policy to be one-to-one. Go through and make sure all the coverages you want are still represented by the new policy. Quotes two and three purported to save me $573 and $468 a year, respectively, but again, those quotes weren't an apples-to-apples comparison with my current policy, as some of the coverages differed. That said, all three quotes were large improvements over my current auto insurance. My current auto policy is bundled with my homeowners insurance and thus linked to my escrow, so I've got some calls to make, but I can safely say I will be using Gabi again soon to find a better bundled policy for auto insurance and home insurance. What We Like About Gabi InsuranceClearly, as someone who has just publicly stated he'll be using Gabi to generate a real quote down the road, I'm a fan. Here's some of what I liked about Gabi:

What We Don't Like About Gabi InsuranceI may be a new Gabi fanboy, but that doesn't mean I'm onboard with the entire experience. Here's where I found the car insurance comparison platform fell short:

What Customers Are Saying About Gabi InsuranceOverall, I had favorable opinions of Gabi, but I wanted to see what other customers were saying about the company. I started with Better Business Bureau and was actually shocked to see that, despite having a BBB rating of an A-, it has an average 1.77 out of 5 stars based on 22 customer reviews. Ouch. Reviews on the Better Business Bureau website were largely around problems with the actual Gabi service, but some have said working with customer service is not a pleasant experience either, whether due to agent miscommunications or just generally slow customer service response time. These poor customer reviews are notably absent on Gabi's site, where it instead shows off its 4.8 out of 5 stars based on "third-party verified reviews" that are certainly not at all curated to paint a favorable picture. Gabi does score well in terms of its mobile app. In the App Store, it currently has a 4.1 rating. I could not easily find it on Google Play. The Bottom LineSo should you try Gabi? If you are actually ready to make the switch to a new car insurance provider and don't mind a little leg work, absolutely. The Zebra is easier since you don't have to relinquish your personal information, but I found The Zebra to be dishonest about its spam policy, frustrating to use and not really much of a money-saver. With Gabi, you'll have to actually take the time to give the platform access to your current policy, but in doing so, big savings and an easy sign-up process could be on the horizon. Timothy Moore is a market research editing and graphic design manager and a freelance writer and editor covering topics on personal finance, travel, careers, education, pet care and automotive. He has worked in the field since 2012 with publications like The Penny Hoarder, Debt.com, Ladders, WDW Magazine, Glassdoor and The News Wheel. This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017. This posting includes an audio/video/photo media file: Download Now |

| Buying These 9 Reusable Products Can Help Save Money Over Time Posted: 14 Apr 2021 07:00 AM PDT Saving the planet doesn't always come cheap. Many of the disposable products we use and love are easier to buy at lower prices than their reusable counterparts. But the convenience of disposable products often comes at a steep cost to the environment. Plastic bags and straws pollute the ocean and end up being ingested by sea animals. Disposable diapers take hundreds of years to decompose in landfills. Reusable products often cost more up front, but you may be surprised to find out how soon they end up paying for themselves since you can use them again and again instead of buying more of the disposable versions. 9 Reusable Products That Will Save You Money Over TimeWe took nine household products, searched for both reusable and disposable versions on Amazon and compared the costs. Here's how they stacked up. Editor's note: The prices in this post are valid as of April 8, 2021. 1. StrawsA stainless steel straw costing $0.50 (or $7.99 for a set of 16), is equal to the cost of about eight disposable straws at 6 cents each. That means that after eight uses, the reusable straw has essentially paid for itself — plus you've got 15 more left over. 2. Water BottlesOne reusable water bottle costing $16.30 is nearly equal to the cost of 20 single-use water bottles at 83 cents each. Translation: Refill your bottle 20 times and then you're done paying for water entirely.  3. Sandwich BagsThis set of 10 reusable, resealable bags costs $13.98, while a box of 150 Ziploc bags runs about $12.99. Think about it this way: You'll only spend about a dollar more for the reusable set, but you'll continue to get use out of them while their throwaway counterparts would just become trash. One reusable bag can be used more than 300 times. 4. DiapersDiaper prices can vary widely. For example, cheap (read: leaky) store-brand diapers cost just a few cents each, while a box of Pampers can set you back nearly $25. The same is true of cloth diapers. For this comparison, take a cloth diaper costing about $4.66 and a disposable diaper at 30 cents each. The cloth diaper has paid for itself after 16 diaper changes. Multiply that over two years of a child's life before potty training, and there are major savings to be had by reusing cloth diapers — many of which are adjustable to keep up with your baby's growth. 5. Paper TowelsOne cloth kitchen towel at $1.50 is less than the cost of one family-sized roll of paper towels at a cost of $2.17 per roll. Enough said. 6. K-CupsDid you even know there was a reusable alternative to those little pods of delectable, life-giving coffee? There totally is! While a box of 40 Starbucks K-Cups will set you back $33.49 (OUCH), a set of four reusable pods that you just refill with your favorite ground coffee runs $9.95.  7. Dryer BallsIf you've never heard of dryer balls, they're little wool balls about the size of a tennis ball that you throw in your dryer with your wet laundry in place of fabric-softening dryer sheets. Because the wool can absorb some moisture from your clothes, manufacturers claim they cut down on energy use and drying time. They can also save you some pennies. A set of six reusable wool dryer balls costs $9.97, while a box of 240 disposable dryer sheets costs just about a dollar less — but you'll have to restock once you use them all. 8. RazorsRazors are synonymous with disposable. A package of 24 of the plastic ones: $18.99. A single chrome reusable safety razor (that will make you feel like Don Draper): $14.66. You do have to replace the blade on the reusable one. Don't worry, they're cheap. A box of 100 is $6.99 — about 7 cents each. 9. Feminine ProductsListen up, gal pals. We're here to tell you that you are not — we repeat, NOT — doomed to pay an exorbitant monthly fee for tampons and liners and pads (not to mention Midol). With a box of 40 tampons costing $12.25 and 66 pads ringing in at $6.38 times every month of your adult life, it's … a lot. So consider this: One pair of Thinx period underwear is $23, and a Diva cup is $32.99. That's a considerable up-front cost, but these products — and really all reusable replacements — are all about long-term savings. Not to mention tossing a little less waste in the landfill. Nicole Dow is a senior writer at The Penny Hoarder. Senior editor Molly Moorhead contributed to this report. This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017. This posting includes an audio/video/photo media file: Download Now |

| You are subscribed to email updates from The Penny Hoarder. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

No comments:

Post a Comment