TechCrunch |

- Tencent helps Chinese students skip prohibitively low speeds for school websites overseas

- Video e-learning platform for MENA, Almentor, closes $6.5M Series B led by Partech

- By working with home entrepreneurs, Jakarta-based DishServe is creating an even more asset-light version of cloud kitchens

- Europe’s cookie consent reckoning is coming

- SVB-led $100M investment makes Chipper Cash Africa’s ‘most valuable startup’

- Intel announces two new 11th-gen chips and a 5G M.2 laptop module at Computex

- Indian health insurance startup Plum raises $15.6 million in Tiger Global-led investment

- Jai Kisan, a fintech startup aimed at rural India, raises $30 million

- Indian logistics giant Delhivery raises $277 million ahead of IPO

- For startups, trustworthy security means going above and beyond compliance standards

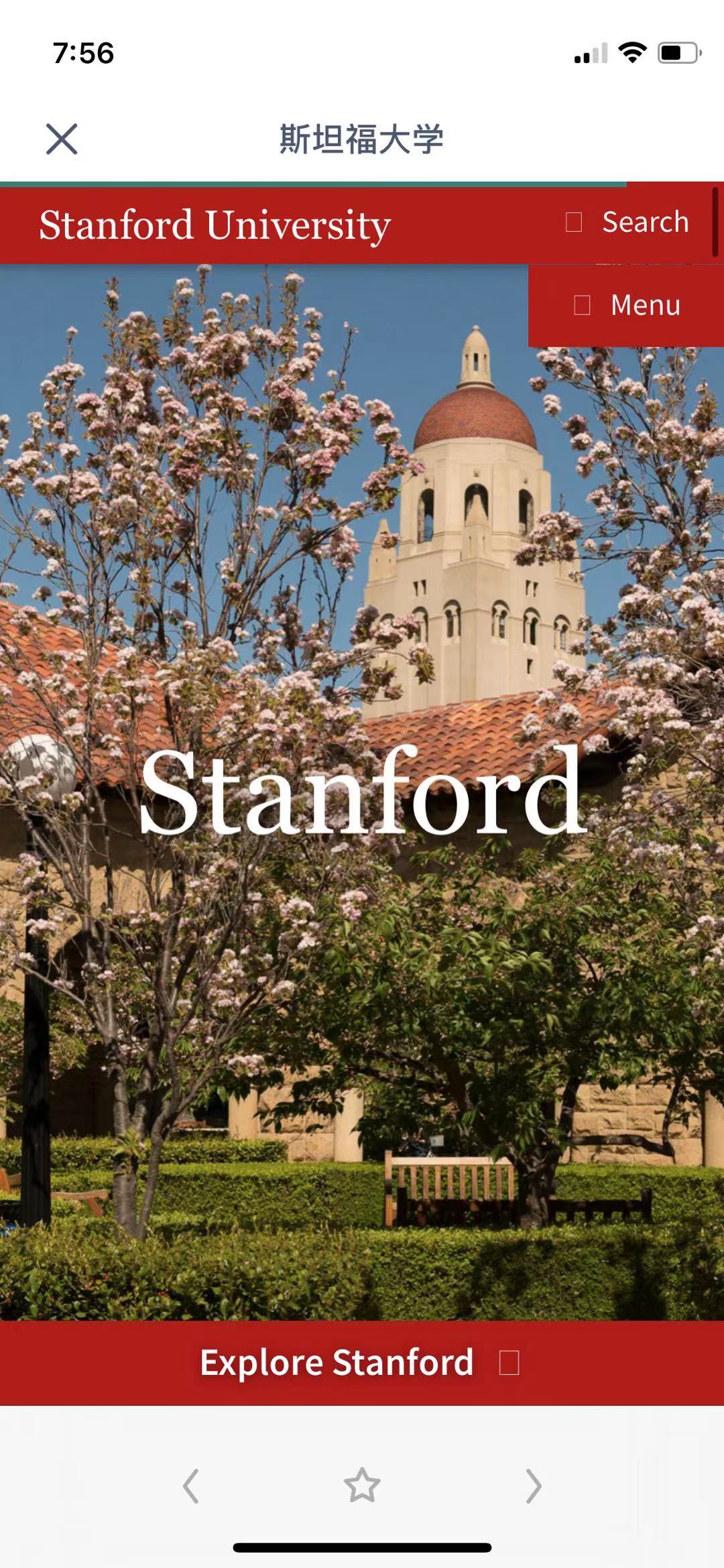

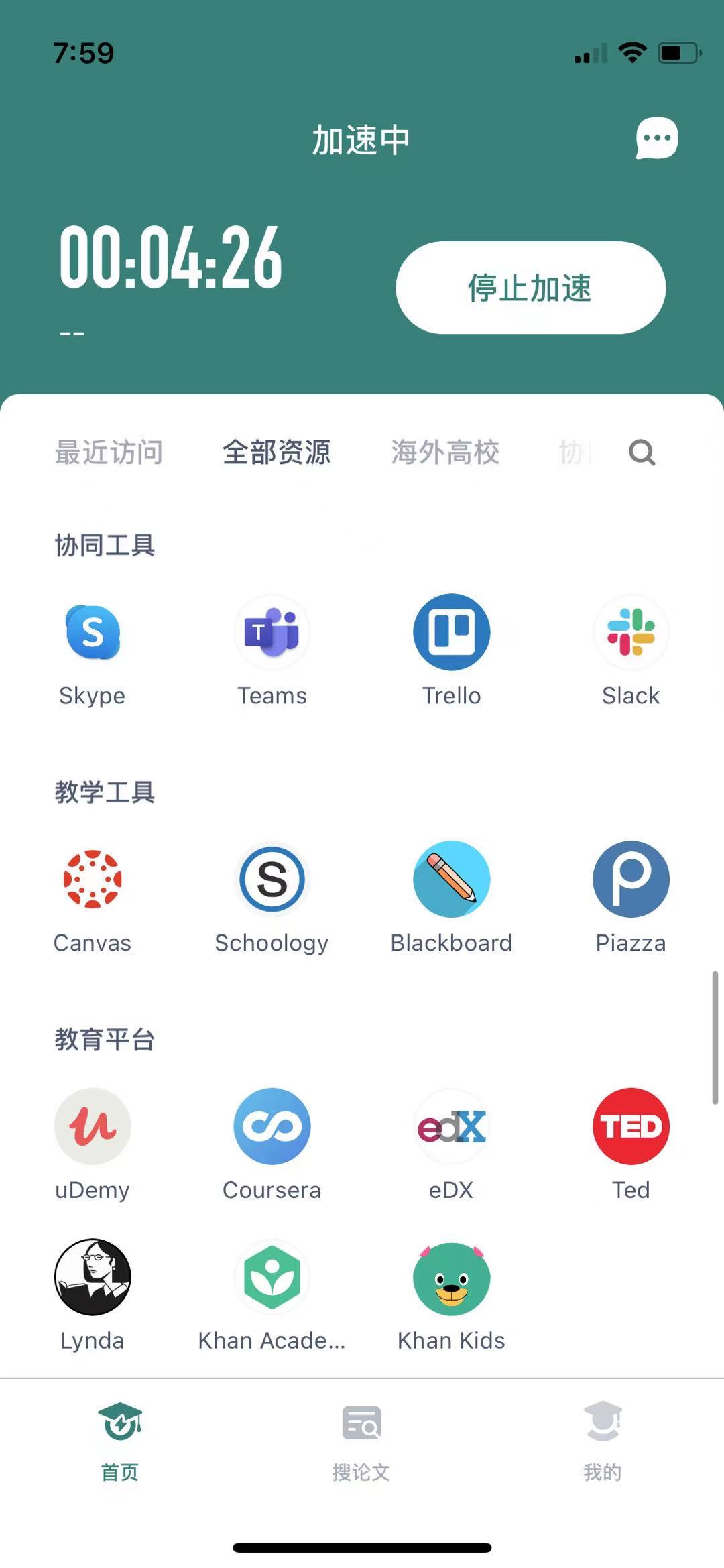

| Tencent helps Chinese students skip prohibitively low speeds for school websites overseas Posted: 31 May 2021 06:44 AM PDT Hundreds of thousands of Chinese students enrolled in overseas schools are stranded as the COVID-19 pandemic continues to disrupt life and airlines worldwide. Learning at home in China, they all face one challenge: Their school websites and other academic resources load excruciatingly slowly because all web traffic has to pass through the country’s censorship apparatus known as the “great firewall.” Spotting a business opportunity, Alibaba’s cloud unit worked on connecting students in China to their university portals abroad through a virtual private network arrangement with American cybersecurity solutions provider Fortinet to provide, Reuters reported last July, saying Tencent had a similar product. Details of Tencent’s offering have come to light. An app called “Chang’e Education Acceleration” debuted on Apple’s App Store in March, helping to speed up loading time for a selection of overseas educational services. It describes itself in a mouthful: “An online learning free accelerator from Tencent, with a mission to provide internet acceleration and search services in educational resources to students and researchers at home and abroad.” Unlike Alibaba’s VPN for academic use, Chang’e is not a VPN, the firm told TechCrunch. The firm didn’t say how it defines VPN or explain how Chang’e works technically. Tencent said Chang’e rolled out on the app’s official website in October. The word “VPN” is a loaded term in China as it often implies illegally bypassing the “great firewall.” People refer to their euphemisms “accelerators” or “scientific internet surfing” otherwise. When Chang’e is switched on, iPhone’s VPN status is shown as “on”, according to a test by TechCrunch.  Tencent’s Chang’e website ‘accelerator’ helps Chinese students stuck home get on their school websites faster. Screenshot: TechCrunch On the welcome page, Chang’e asks users to pick from eight countries, including the U.S., Canada, and the U.K., for “acceleration”. It also shows the latency time and expected speed increased for each region. Once a country is picked, Chang’e shows a list of educational resources that users can visit on the app’s built-in browser. They include the websites of 79 top universities, mostly U.S. and the U.K. ones; team collaboration tools like Microsoft Teams, Trello and Slack; remote-learning platforms UDemy, Coursera, Lynda and Khan Academy; research networks such as SSRN and JSTOR; programming and engineering communities like Stack Overflow, Codeacademy and IEEE; economics databases from the World Bank and OECD; as well as resources for medical students like PubMed and Lancet. Many of these services are not blocked in China but load slowly on mainland China behind the “great firewall.” Users can request sites not already on the list to be included.  Accessing Stanford’s website through Chang’e. Screenshot: TechCrunch Chang’e appears to have whitelisted only its chosen sites rather than all traffic on a user’s smartphone. Google, Facebook, YouTube and other websites banned in China are still unavailable when the Chang’e is at work. The app, available on both Android and iOS for free, doesn’t currently require users to sign up, a rare gesture in a country where online activities are strictly regulated and most websites ask for users’ real-name registrations.  Services accessible through Chang’e. Screenshot: TechCrunch The offerings from Alibaba and Tencent are indicative of the inadvertent consequences caused by Beijing’s censorship system designed to block information deemed illegal or harmful to China’s national interest. Universities, research institutes, multinational corporations and exporters are often forced to seek censorship circumvention apps for what the authorities would consider innocuous purposes. VPN providers have to obtain the government’s green light to legally operate in China and users of licensed VPN services are prohibited from browsing websites thought of us endangering China’s national security. In 2017, Apple removed hundreds of unlicensed VPN apps from its China App Store at Beijing’s behest. In October, TechCrunch reported that the VPN app and browser Tuber gave Chinese users a rare glimpse into the global internet ecosystem of Facebook, YouTube, Google and other mainstream apps, but the app was removed shortly after the article was published. |

| Video e-learning platform for MENA, Almentor, closes $6.5M Series B led by Partech Posted: 31 May 2021 12:13 AM PDT There are more than 400 million Arabic speakers globally and that number isn’t slowing down anytime soon. Arabic, to most people, is a tough language even to those who speak it. According to Duolingo, someone fluent in Egyptian Arabic might not fully understand Yemeni Arabic speakers because of the vast difference in dialect. While individuals can easily navigate dialects, it can be relatively hard for them to find tailored Arabic content essential for everyday life. Dr Ihab Fikry and Ibrahim Kamel founded Almentor.net in 2016 as an online video learning platform to compensate for this lack of online learning content for Arabic speakers. In collaboration with hundreds of leaders, educators, and experts, the platform offers courses and talks in various fields like health, humanities, technology, entrepreneurship, business management, lifestyle, drama, sports, corporate communication, and digital media. In 2016, Almentor closed a $3.5 million seed round and two years ago raised $4.5 million Series A led by Egypt’s Sawari Ventures. With this Series B investment, the Dubai-based edtech company has raised $14.5 million in total. San Francisco and Paris-based VC firm Partech led the financing round with participation from Sawari Ventures, fellow Series A investor Egypt Ventures, and Sango Capital. Almentor provides Arab learners with the necessary skills crucially needed to advance their professional careers and personal lives. The platform claims to have the biggest continuous learning library in the region and one of the biggest worldwide. With offices in Dubai, Cairo, and Saudi Arabia, its video content is developed in-house and made in Arabic and English. “The vision and reason behind starting Almentor is we understand that in our region of more than 100 million people, of which 90% cannot properly learn with any other language other than Arabic,” Fikry said to TechCrunch. “So we wanted to have a cutting-edge state of the art platform that will change people’s ideology and help them be objective, and focus based on topics that can be taught as prodigious learning.” For first-time products like Almentor, it can be hard to get both investors and customers on board. According to CEO Fikry, the first challenge was to convince the investment community in the MENA region that Almentor was creating a new industry in video e-learning that “had lots of potential to power tools in the region.” Almentor’s business is an intersection of education, media, and technology. Its offerings are dissected into three: the flagship B2C product, a white-label B2B model for blue-chip companies, and the last, which Fikry calls the ‘special project’ for governmental bodies. For its B2C product, Almentor sells courses to users for $20-$30 of which they get to keep for a lifetime. Fikry says that in June, the company is planning to introduce a subscription-based model where users can have unlimited access to all of its 12,000 video content for a fee to its more than 1 million registered users.

The B2B model is where Almentor opens its library to companies to customize their content for employees. These videos are mainly tutorials or training needed to thrive at work, and since 2016, Almentor has executed 78 deals with partner companies. The special project’s model highlights Almentor’s work with the government. One time, the company had a partnership with the Egyptian government to upskill the country’s movie industry. It has completed 11 more similar special projects since launching five years ago. Across all three models, Fikry says Almentor has successfully delivered more than 2 million learning experiences. With this investment, the company wants to improve content production and quality and educate people in the MENA region on why they need the product. "We are now leading the continuous video learning industry in the Arab region, and we have a responsibility that goes beyond our ambitions for Almentor. Our responsibility now is to work unceasingly to improve the industry as a whole in the Arab region, and this can only be achieved through gaining the confidence of the Arab learners in the value, professionalism and impartiality of the content provided by the platform and working in line with the global learning trends." Speaking on the investment for Partech, general partner Cyril Collon said: "Since our first interaction, we have been very impressed by Ihab and Ibrahim, two fantastic mission-driven entrepreneurs who have been executing on a bold vision since 2016, and who built the leading Arabic self-learning go-to content provider in the Middle East and Africa. We are looking forward to supporting the company in its next phase of growth to serve the 430 million Arabic-speaking population and expand access to on-demand cutting-edge personal learning & developments options." |

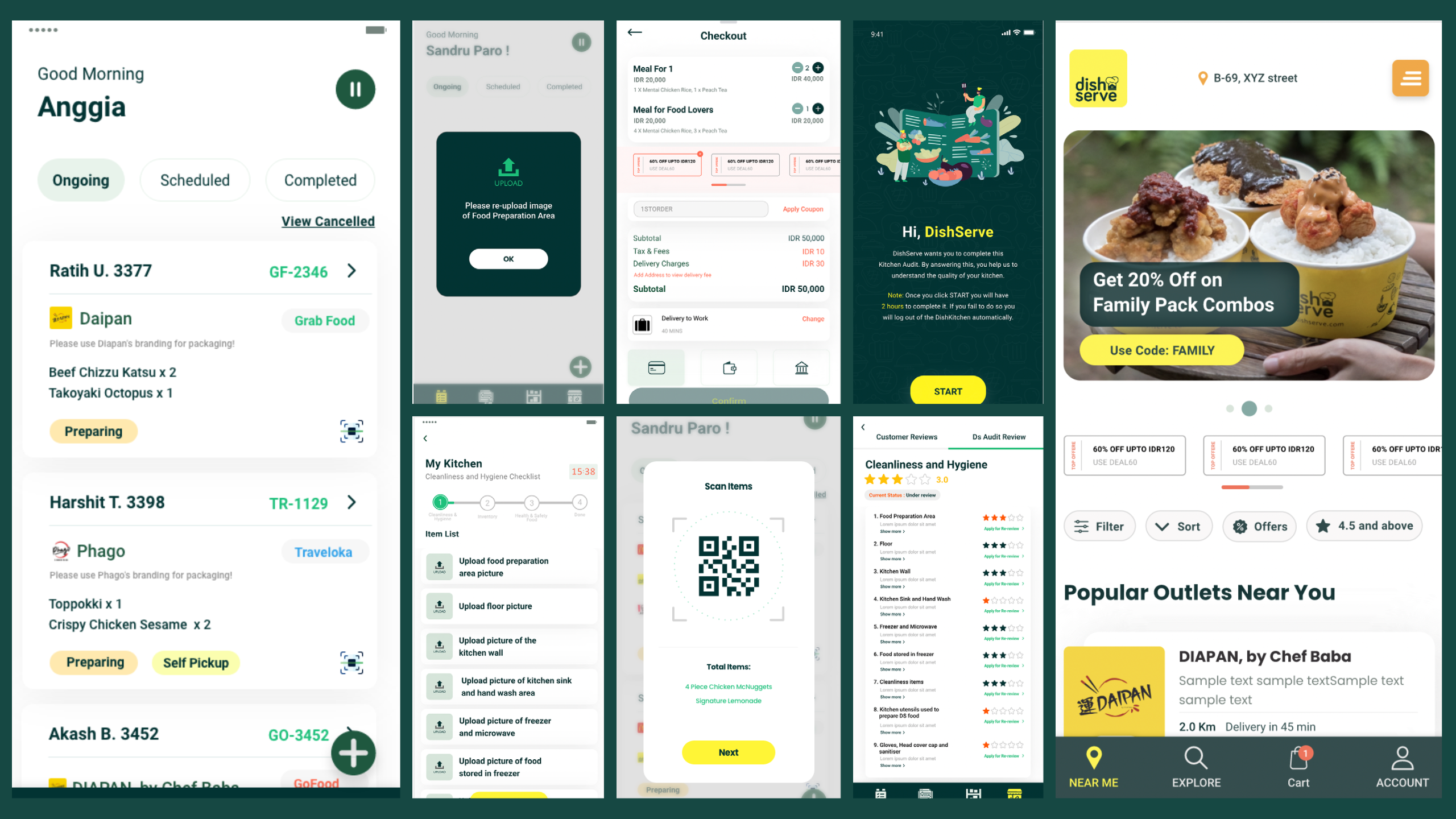

| Posted: 30 May 2021 10:38 PM PDT Cloud kitchens are already meant to reduce the burden of infrastructure on food and beverage brands by providing them with centralized facilities to prepare meals for delivery. This means the responsibility falls on cloud kitchen operators to make sure they have enough locations to meet demand from F&B clients, while ensuring fast deliveries to end customers. Indonesian network DishServe has figured out a way to make running cloud kitchen networks even more asset-light. Launched by budget hotel startup RedDoorz's former chief operating officer, DishServe partners with home kitchens instead of renting or buying its own facilities. It currently works with almost 100 home kitchens in Jakarta, and focuses on small- to medium-sized F&B brands, serving as their last-mile delivery network. Launched in fall 2020, DishServe has raised an undisclosed amount of pre-seed funding from Insignia Ventures Partners. DishServe was founded in September 2020 by Rishabh Singhi. After leaving RedDoorz at the end of 2019, Singhi moved to New York, with plans to launch a new hospitality startup that could quickly convert any commercial space into members' clubs like Soho House. The nascent company had already created sample pre-fabricated rooms and was about to start leasing property when the COVID-19 lockdown hit New York City in March 2020. Singhi said he went on a "soul searching spree" for a couple of months, deciding what to do and if he should return to Southeast Asia. He realized that since many restaurants had to switch to online orders and delivery to survive the pandemic, this could potentially be an equalizer for small F&B brands that compete with larger players, like McDonald's. But lockdowns meant that a lot of people had to pick from a limited range of restaurants close to where they lived. At the same time, Singhi saw that there were a lot of people who wanted to make more money, but couldn't work outside of their homes, like stay-at-home moms. DishServe was created to connect all three sides: F&B brands that want to expand without spending a lot of money, home entrepreneurs and diners hungry for more food options. Its other founders include Stefanie Irma, an early RedDoorz employee who served as its country head for the Philippines; serial entrepreneur Vinav Bhanawat; and Fathhi Mohamed, who also co-founded Sri Lankan on-demand taxi service PickMe. The company works with F&B brands that typically have between just one to 15 retail locations, and want to increase their deliveries without opening new outlets. DishServe's clients also include cloud kitchen companies who use its home kitchen network for last-mile distribution to expand their delivery coverage and catering services. "The brands don't to have to incur any upfront costs, and it's a cheaper way to distribute as well because they don't have to pay for electricity, plumbing and other things like that," said Singhi. "And for agents, it gives them a chance to earn money from their homes." How it worksBefore adding a home kitchen to its network, DishServe screens applicants by asking them to send in a series of photos, then doing an in-person check. If a kitchen is accepted, DishServe upgrades it so it has the same equipment and functionality as the other home kitchens in its network. The company covers the cost of the conversion process, which usually takes about three hours and costs $500 USD, and maintains ownership of the equipment, taking it back if a kitchen decided to stop working with DishServe. Singhi said DishServe is usually able to recover the cost of a conversion four months after a kitchen begins operating. Home kitchens start out by serving DishServe's own white-label brand as a trial run before it opens to other brands. Each can serve up to three additional brands at a time. One important thing to note is that DishServe's home kitchens, which are usually run by one person, don't actually cook any food. Ingredients are provided by F&B brands, and home kitchen operators follow a standard set of procedures to heat, assemble and package meals for pick-up and delivery.  Screenshots of DishServe’s apps for home kitchen operators and customers DishServe makes sure standard operating procedures and hygiene standards are being maintained through frequent online audits. Agents, or kitchen operators, regularly submit photos and videos of kitchens based on a checklist (i.e. food preparation area, floors, walls, hand-washing area and the inside of their freezers). Singhi said about 90% of its agents are women between the ages of 30 to 55, with an average household income of $1,000. By working with DishServe, they typically make an additional $600 a month once their kitchen is operating at full capacity with four brands. DishServe monetizes through a revenue-sharing model, charging F&B brands and splitting that with its agents. After joining DishServe, F&B brands pick what home kitchens they want to work with, and then distribute ingredients to kitchens, using DishServe's real-time dashboard to monitor stock. Some ingredients have a shelf life of up to six months, while perishables, like produce, dairy and eggs, are delivered daily. DishServe's "starter pack" for onboarding new brands lets them pick pick five kitchens, but Singhi said most brands usually begin with between 10 to 20 kitchens so they can deliver to more spots in Jakarta and save money by preparing meals in bulk. DishServe plans to focus on growing its network in Jakarta until at least the end of this year, before expanding into other cities. "One thing we are trying to change about the F&B industry is that instead of highly-concentrated, centralized food business, like what exists today, we are decentralizing it by enabling micro-entrepreneurs to act as a distribution network," Singhi said. |

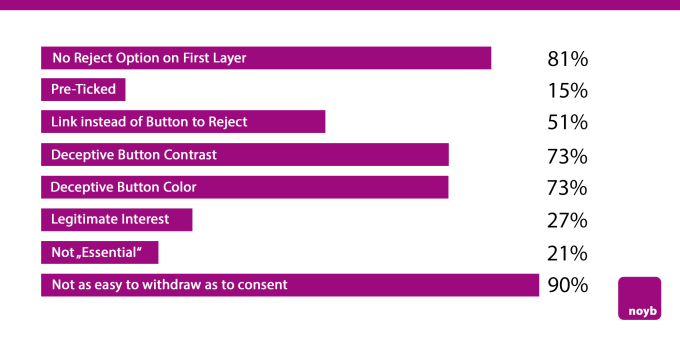

| Europe’s cookie consent reckoning is coming Posted: 30 May 2021 10:00 PM PDT Cookie pop-ups getting you down? Complaints that the web is ‘unusable’ in Europe because of frustrating and confusing ‘data choices’ notifications that get in the way of what you’re trying to do online certainly aren’t hard to find. What is hard to find is the ‘reject all’ button that lets you opt out of non-essential cookies which power unpopular stuff like creepy ads. Yet the law says there should be an opt-out clearly offered. So people who complain that EU ‘regulatory bureaucracy’ is the problem are taking aim at the wrong target. EU law on cookie consent is clear: Web users should be offered a simple, free choice — to accept or reject. The problem is that most websites simply aren’t compliant. They choose to make a mockery of the law by offering a skewed choice: Typically a super simple opt-in (to hand them all your data) vs a highly confusing, frustrating, tedious opt-out (and sometimes even no reject option at all). Make no mistake: This is ignoring the law by design. Sites are choosing to try to wear people down so they can keep grabbing their data by only offering the most cynically asymmetrical ‘choice’ possible. However since that’s not how cookie consent is supposed to work under EU law sites that are doing this are opening themselves to large fines under the General Data Protection Regulation (GDPR) and/or ePrivacy Directive for flouting the rules. See, for example, these two whopping fines handed to Google and Amazon in France at the back end of last year for dropping tracking cookies without consent… While those fines were certainly head-turning, we haven’t generally seen much EU enforcement on cookie consent — yet. This is because data protection agencies have mostly taken a softly-softly approach to bringing sites into compliance. But there are signs enforcement is going to get a lot tougher. For one thing, DPAs have published detailed guidance on what proper cookie compliance looks like — so there are zero excuses for getting it wrong. Some agencies had also been offering compliance grace periods to allow companies time to make the necessary changes to their cookie consent flows. But it’s now a full three years since the EU’s flagship data protection regime (GDPR) came into application. So, again, there’s no valid excuse to still have a horribly cynical cookie banner. It just means a site is trying its luck by breaking the law. There is another reason to expect cookie consent enforcement to dial up soon, too: European privacy group noyb is today kicking off a major campaign to clean up the trashfire of non-compliance — with a plan to file up to 10,000 complaints against offenders over the course of this year. And as part of this action it’s offering freebie guidance for offenders to come into compliance. Today it’s announcing the first batch of 560 complaints already filed against sites, large and small, located all over the EU (33 countries are covered). noyb said the complaints target companies that range from large players like Google and Twitter to local pages “that have relevant visitor numbers”. "A whole industry of consultants and designers develop crazy click labyrinths to ensure imaginary consent rates. Frustrating people into clicking 'okay' is a clear violation of the GDPR's principles. Under the law, companies must facilitate users to express their choice and design systems fairly. Companies openly admit that only 3% of all users actually want to accept cookies, but more than 90% can be nudged into clicking the 'agree' button,” said noyb chair and long-time EU privacy campaigner, Max Schrems, in a statement. "Instead of giving a simple yes or no option, companies use every trick in the book to manipulate users. We have identified more than fifteen common abuses. The most common issue is that there is simply no 'reject' button on the initial page,” he added. "We focus on popular pages in Europe. We estimate that this project can easily reach 10,000 complaints. As we are funded by donations, we provide companies a free and easy settlement option — contrary to law firms. We hope most complaints will quickly be settled and we can soon see banners become more and more privacy friendly." To scale its action, noyb developed a tool which automatically parses cookie consent flows to identify compliance problems (such as no opt out being offered at the top layer; or confusing button coloring; or bogus ‘legitimate interest’ opt-ins, to name a few of the many chronicled offences); and automatically create a draft report which can be emailed to the offender after it’s been reviewed by a member of the not-for-profit’s legal staff. It’s an innovative, scalable approach to tackling systematically cynical cookie manipulation in a way that could really move the needle and clean up the trashfire of horrible cookie pop-ups. noyb is even giving offenders a warning first — and a full month to clean up their ways — before it will file an official complaint with their relevant DPA (which could lead to an eye-watering fine). Its first batch of complaints are focused on the OneTrust consent management platform (CMP), one of the most popular template tools used in the region — and which European privacy researchers have previously shown (cynically) provides its client base with ample options to set non-compliant choices like pre-checked boxes… Talk about taking the biscuit. A noyb spokeswoman said it’s started with OneTrust because its tool is popular but confirmed the group will expand the action to cover other CMPs in the future. The first batch of noyb’s cookie consent complaints reveal the rotten depth of dark patterns being deployed — with 81% of the 500+ pages not offering a reject option on the initial page (meaning users have to dig into sub-menus to try to find it); and 73% using “deceptive colors and contrasts” to try to trick users into clicking the ‘accept’ option. noyb’s assessment of this batch also found that a full 90% did not provide a way to easily withdraw consent as the law requires.  Cookie compliance problems found in the first batch of sites facing complaints (Image credit: noyb) It’s a snapshot of truly massive enforcement failure. But dodgy cookie consents are now operating on borrowed time. Asked if it was able to work out how prevalent cookie abuse might be across the EU based on the sites it crawled, noyb’s spokeswoman said it was difficult to determine, owing to technical difficulties encountered through its process, but she said an initial intake of 5,000 websites was whittled down to 3,600 sites to focus on. And of those it was able to determine that 3,300 violated the GDPR. That still left 300 — as either having technical issues or no violations — but, again, the vast majority (90%) were found to have violations. And with so much rule-breaking going on it really does require a systematic approach to fixing the ‘bogus consent’ problem — so noyb’s use of automation tech is very fitting. More innovation is also on the way from the not-for-profit — which told us it’s working on an automated system that will allow Europeans to “signal their privacy choices in the background, without annoying cookie banners”. At the time of writing it couldn’t provide us with more details on how that will work (presumably it will be some kind of browser plug-in) but said it will be publishing more details “in the next weeks” — so hopefully we’ll learn more soon. A browser plug-in that can automatically detect and select the ‘reject all’ button (even if only from a subset of the most prevalent CMPs) sounds like it could revive the ‘do not track’ dream. At the very least, it would be a powerful weapon to fight back against the scourge of dark patterns in cookie banners and kick non-compliant cookies to digital dust.

|

| SVB-led $100M investment makes Chipper Cash Africa’s ‘most valuable startup’ Posted: 30 May 2021 10:00 PM PDT Fintech in Africa is a goldmine. Investors are betting big on startups offering a plethora of services from payments and lending to neobanks, remittances and cross-border transfers, and rightfully so. Each of these services solves unique sets of challenges. For cross-border payments, it’s the outrageous rates and regulatory hassles involved with completing transactions from one African country to another. Chipper Cash, a three-year-old startup that facilitates cross-border payment across Africa, has closed a $100 million Series C round to introduce more products and grow its team. It hasn’t been too long ago since Chipper Cash was last in the news. In November 2020, the African cross-border fintech startup raised $30 million Series B led by Ribbit Capital and Jeff Bezos fund Bezos Expeditions. This was after closing a $13.8 million Series A round from Deciens Capital and other investors in June 2020. Hence, Chipper Cash has gone through three rounds totalling $143.8 million in a year. However, when the $8.4 million raised in two seed rounds back in 2019 is included, this number increases to $152.2 million. SVB Capital, the investment arm of U.S. high-tech commercial bank Silicon Valley Bank led this Series C round. Others who participated in this round include existing investors — Deciens Capital, Ribbit Capital, Bezos Expeditions, One Way Ventures, 500 Startups, Tribe Capital, and Brue2 Ventures. Chipper Cash was launched in 2018 by Ham Serunjogi and Maijid Moujaled. The pair met in Iowa after coming to the U.S. for studies. Following their stints at big names like Facebook, Flickr and Yahoo!, the founders decided to work on their own startup. Last year, the company which offers mobile-based, no fee, P2P payment services, was present in seven countries: Ghana, Uganda, Nigeria, Tanzania, Rwanda, South Africa and Kenya. Now, it has expanded to a new territory outside Africa. “We’ve expanded to the U.K., it’s the first market we’ve expanded to outside Africa,” CEO Serunjogi said to TechCrunch. In addition and as a sign of growth, the company which boasts more than 200 employees plans to increase its workforce by hiring 100 staff throughout the year. The number of users on Chipper Cash has increased to 4 million, up 33% from last year. And while the company averaged 80,000 transactions daily in November 2020 and processed $100 million in payments value in June 2020, it is unclear what those figures are now as Serunjogi declined to comment on them, including its revenues. When we reported its Series B last year, Chipper Cash wanted to offer more business payment solutions, cryptocurrency trading options, and investment services. So what has been the progress since then? “We’ve launched cards products in Nigeria and we’ve also launched our crypto product. We’re also launching our US stocks product in Uganda, Nigeria and a few other countries soon,” Serunjogi answered. Crypto is widely adopted in Africa. African users are responsible for a sizeable chunk of transactions that take place on some global crypto-trading platforms. For instance, African users accounted for $7 billion of the $8.3 billion in Luno’s total trading volume. Binance P2P users in Africa also grew 2,000% within the past five months while their volumes increased by over 380%. Individuals and small businesses across Nigeria, South Africa and Kenya account for most of the crypto activity on the continent. Chipper Cash is active in these countries and tapping into this opportunity is basically a no brainer. “Our approach to growing products and adding products is based on what our users find valuable. As you can imagine, crypto is one technology that has been widely adopted in Africa and many emerging markets. So we want to give them the power to access crypto and to be able to buy, hold, and sell crypto whenever,” the CEO added.

However, its crypto service isn’t available in Nigeria, the largest crypto market in Africa. The reason behind this is the Central Bank of Nigeria’s (CBN) regulation on crypto activities in the country prohibiting users from converting fiat into crypto from their bank accounts. To survive, most crypto players have adopted P2P methods but Chipper Cash isn’t offering that yet and according to Serunjogi, the company is “looking forward to any development in Nigeria that allows it to be offered freely again.” The same goes for the investment service Chipper Cash plans to roll out in Nigeria and Uganda soon. Presently, Nigeria's capital market regulator SEC is keeping tabs on local investment platforms and bringing their activities under its purview. Chipper Cash will not be exempt when the product is live in Nigeria and has begun engaging regulators to be ahead of the curve. “As fintech explodes and as innovation continues to move forward, consumers have to be protected. We invest millions of dollars every year in our compliance programs, so I think working closely with the regulators directly so that these products are offered in a compliant manner is important,” Serunjogi noted. Six billion-dollar companies in Africa; the fifth fintech unicorn?During our call, Serunjogi made some remarks about Nigeria’s central bank which resembles comments made by Flutterwave CEO Olugbenga Agboola back in March. While acknowledging the central banks in Kenya, Rwanda, Uganda for creating environments where innovation can thrive, he said: “Nigeria has probably the most exciting and vibrant tech ecosystem in Africa. And that’s credit directly to CBN for creating and fostering an environment that allowed multiple startups like ourselves and others like Flutterwave to blossom.” Most fintechs would argue that the CBN stifles innovation but comments from both CEOs seems to suggest otherwise. From all indication, Chipper Cash and Flutterwave strive to be on the right side of the country’s apex bank policies and regulations. It is why they are one of the fastest-growing fintechs in the region and also billion-dollar companies. “Obviously, we’re not getting into our valuation, but we’re probably the most valuable private startup in Africa today after this round. So that’s a reflection of the environment that regulators like CBN have created to allowed innovation and growth,” Serunjogi commented when asked about the company’s valuation. Up until last week, the only private unicorn startup in Africa this year was Flutterwave. Then China-backed and African-focused fintech OPay came along as the company was reported to be in the process of raising $400 million at a $1.5 billion valuation. If Serunjogi’s comment is anything to go by, Chipper Cash might currently be valued between $1-2 billion thus joining the exclusive billion-dollar club. But to be sure, I asked Serunjogi again if the company is indeed a unicorn. This time, he gave a more cryptic answer. “We’re not commenting on the size of our valuation publicly. One of the things that I’ve been quite keen on internally and externally is that the valuation of our company has not been a focus for us. It’s not a goal we’re aspiring to achieve. For us, the thing that drives us is that we have a product that is impactful to our users.”  Maijid Moujaled (CTO) and Ham Serunjogi (CEO) Serunjogi added that this investment actualizes the importance of possessing a solid balance sheet and onboarding SVB Capital and getting existing investors to double down is a means to that end. According to him, a strong balance sheet will provide the infrastructure needed to support key long-term investments which will translate to more exciting products down the road. “We look at our investors as key partners to the business. So having very strong partners around the table makes us a stronger company. These are partners who can put capital into our business, and we’re also able to learn from them in several other ways,” he said of the investors backing the three-year-old company. Just like Ribbit Capital and Bezos Expeditions in last year’s Series B, this is SVB Capital’s first foray into the African market. In an email, the managing director of SVB Capital Tilli Bannett, confirmed the fund’s investment in Chipper Cash. According to her, the VC firm invested in Chipper Cash because it has created an easy and accessible way for people living in Africa to fulfil their financial needs through enhanced products and user experiences. “As a result, Chipper has had a phenomenal trajectory of consumer adoption and volume through the product. We are excited at the role Chipper has forged for itself in fostering financial inclusion across Africa and the vast potential that still lies ahead,” she added. Fintech remains the bright spot in African tech investment. In 2020, the sector accounted for more than 25% of the almost $1.5 billion raised by African startups. This figure will likely increase this year as four startups have raised $100 million rounds already: TymeBank in February, Flutterwave in March, and OPay and Chipper Cash this May. All except TymeBank are now valued at over $1 billion, and it becomes the first time Africa has witnessed two or more billion-dollar companies in a year. In addition to Jumia (e-commerce), Interswitch (fintech), and Fawry (fintech), the continent now has six billion-dollar tech companies. Here’s another interesting piece of information. The timeframe at which startups are reaching this landmark seems to be shortening. While it took Interswitch and Fawry seventeen and thirteen years respectively, it took Flutterwave five years; Jumia, four years; then OPay and Chipper Cash three years. We reached out to the VC firm for comment regarding Chipper Cash’s valuation. |

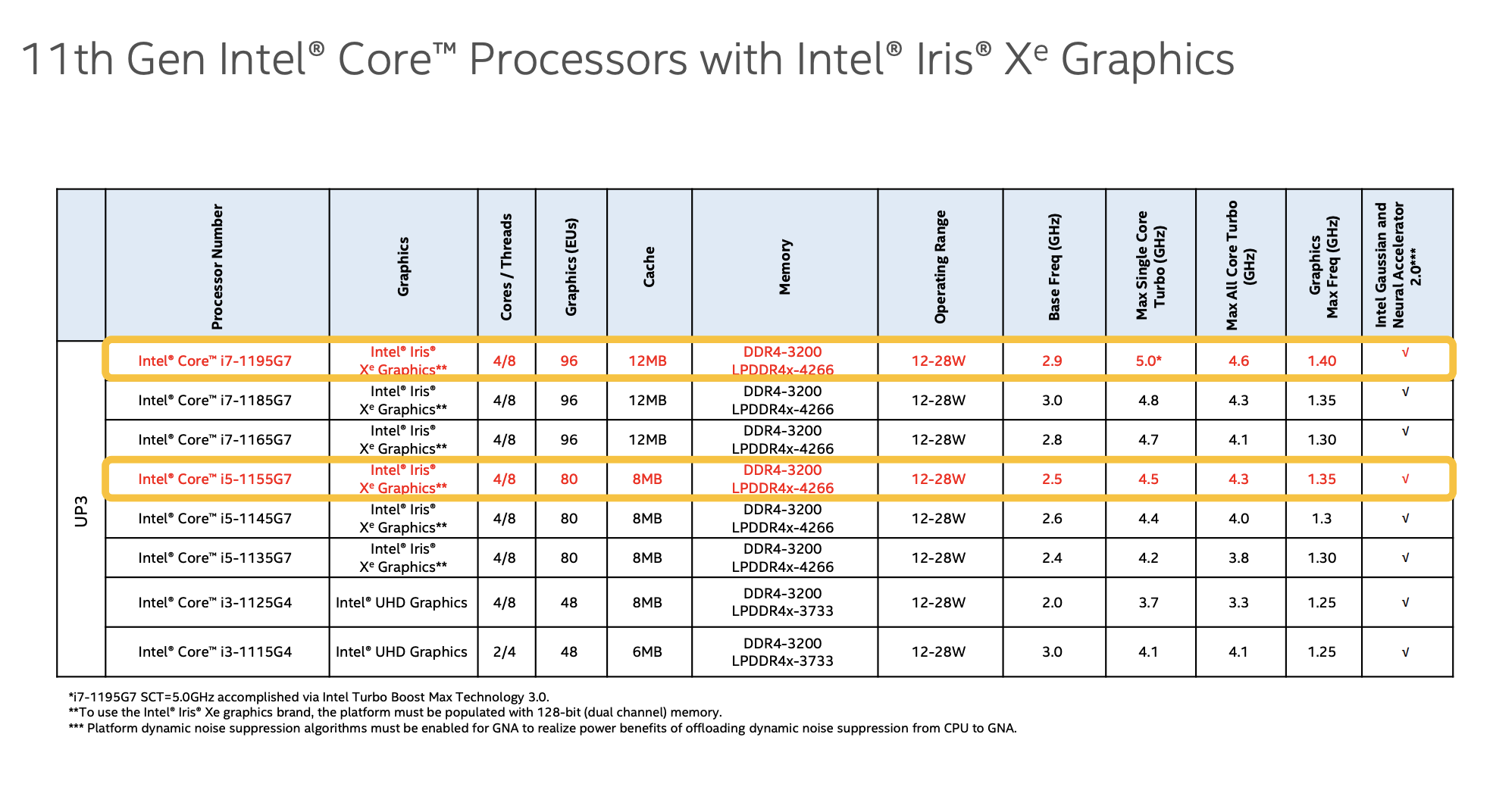

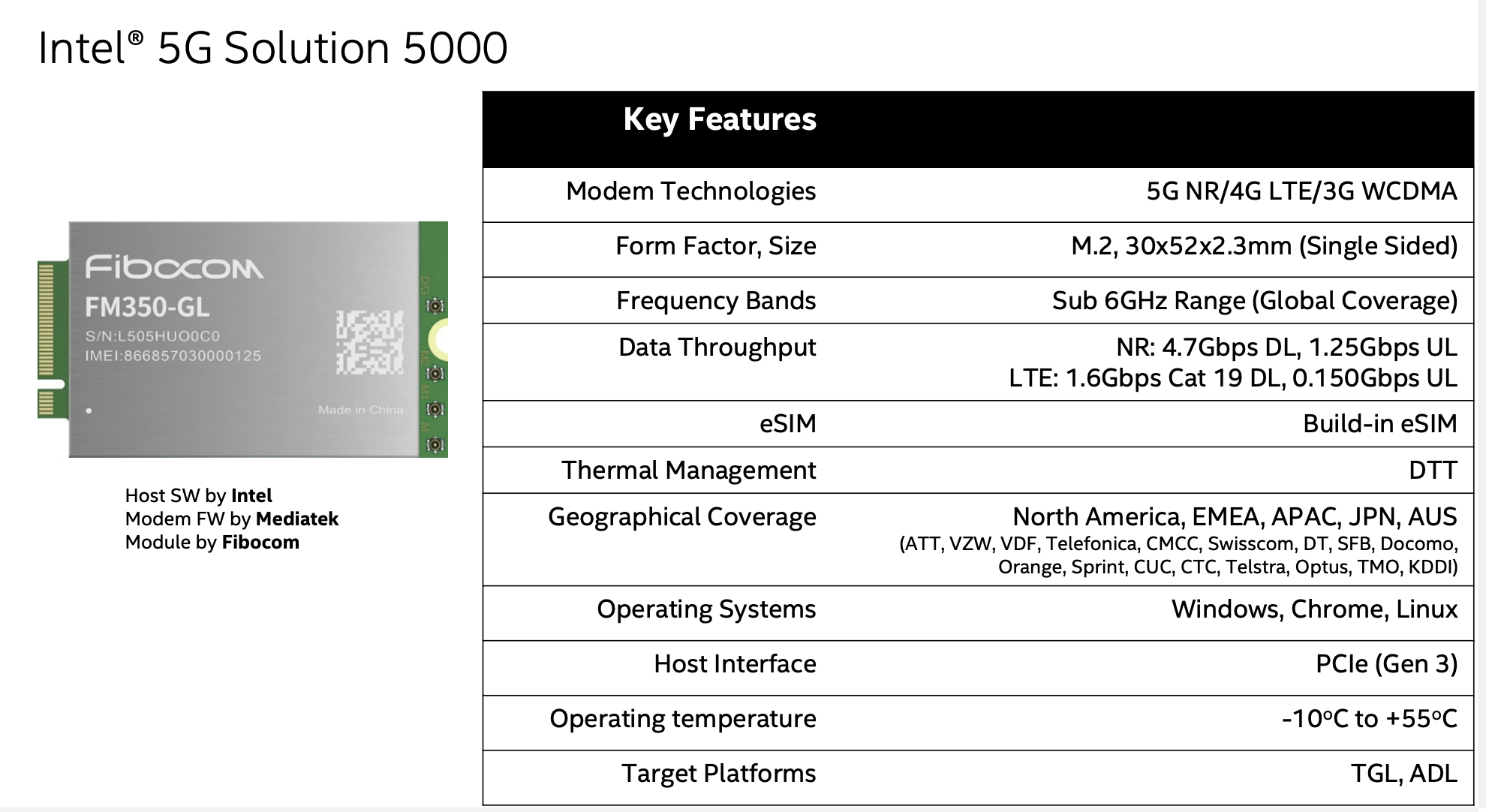

| Intel announces two new 11th-gen chips and a 5G M.2 laptop module at Computex Posted: 30 May 2021 09:47 PM PDT Intel kicked off this year's virtual Computex by announcing two new 11th Gen U-Series chips for use in thin, lightweight laptops. It also unveiled its first 5G M.2 module for laptops, designed in a partnership with MediaTek (Intel sold its smartphone modem business to Apple in 2019). Both of Intel's new chips have Intel Irix Xe graphics. The flagship model is the Core i7-1195G7, which has base clock speed is 2.9 GHz, but can reach up to 5.0 GHz on a single core using Intel's Turbo Boost Max 3.0 tech. The other chip, called the Core i5-1155G7, has a base clock speed of 2.5GHzm and a maximum of 4.5GHz. Both chips have four cores and eight threads.  A comparison chart of Intel’s new 11th-gen chips The 5G M.2 module, called the "5G Solution 5000," supports 5G NR midband, sub-6GHz frequencies and eSIM tech. Intel has partnerships with telecoms in North America, EMEA, APAC, Japan and Australia. The module is expected to be in laptops produced by Acer, ASUS, HP and other manufacturers by the end of this year, and OEMs are also working on 250 designs based on 11th Gen U-Series chips, expected to hit the market by the holidays.  Specs for Intel’s new 5G M.2 module

|

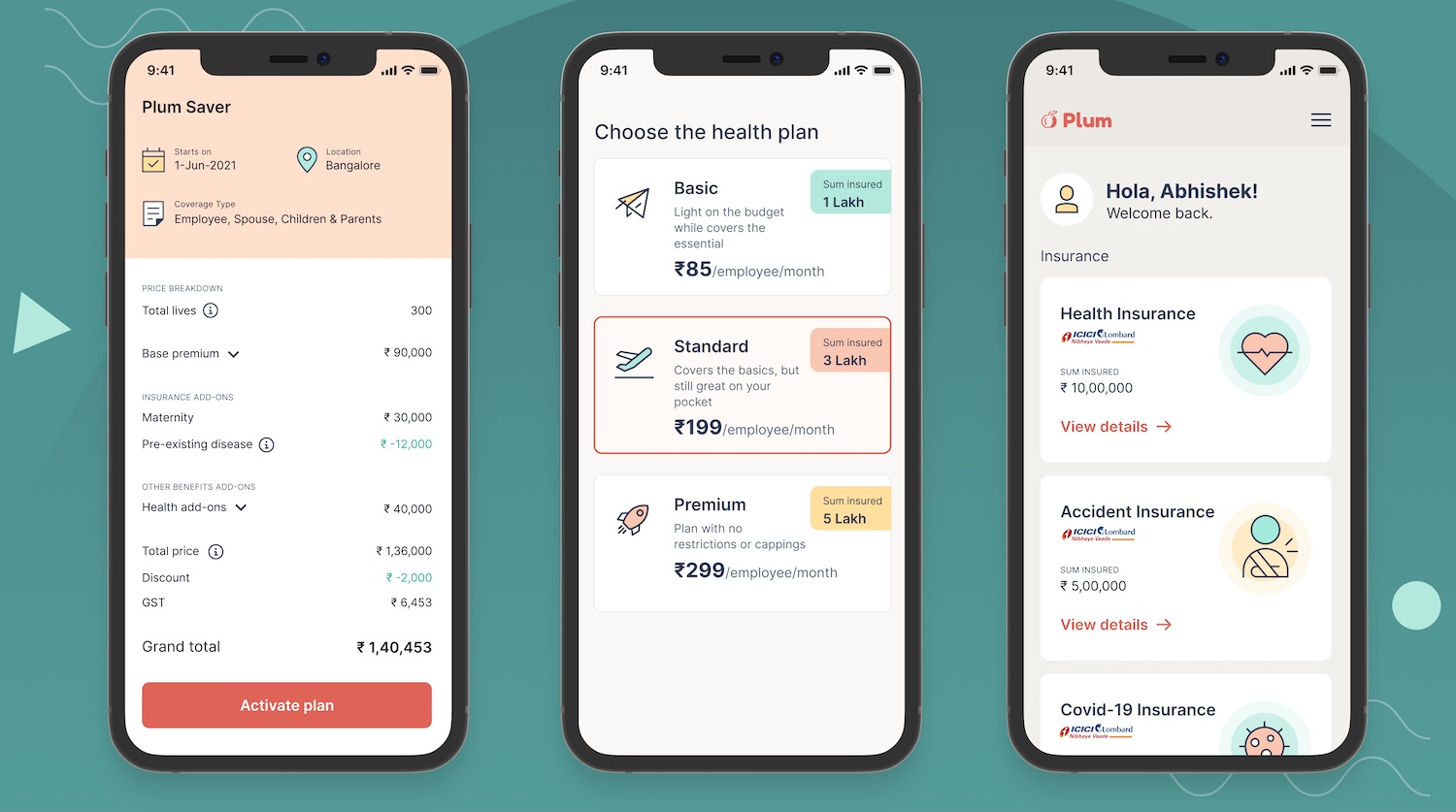

| Indian health insurance startup Plum raises $15.6 million in Tiger Global-led investment Posted: 30 May 2021 09:37 PM PDT The vast majority of people in India, the world's second most populous nation, don't have health insurance coverage. A significant portion of the population that does have coverage get it from their employers. Plum, a young startup that is making it easier and more affordable for more firms in the nation to provide insurance coverage to their employees, said on Monday it has raised $15.6 million in its Series A funding to accelerate its growth. Tiger Global led the new funding round, with participation from existing investors Sequoia Capital India's Surge, Tanglin Venture Partners, Incubate Fund, and Gemba Capital. TechCrunch reported earlier this year that Plum was in talks with Tiger Global for the new financing round. Kunal Shah (founder of Cred), Gaurav Munjal, Roman Saini and Hemesh Singh (founders of Unacademy), Lalit Keshre, Harsh Jain and Ishan Bansal (founders of Groww), Ramakant Sharma and Anuj Srivastava (founders of Livspace), and Douglas Feirstein (founder of Hired) also participated in the new round, which brings one-a-half-year-old startup's to-date raise to $20.6 million. Plum offers health insurance coverage on a B2B2C model. The startup partners with small businesses to provide health insurance coverage to all their employees (and their family members), charging as little as $1 a month for an employee.

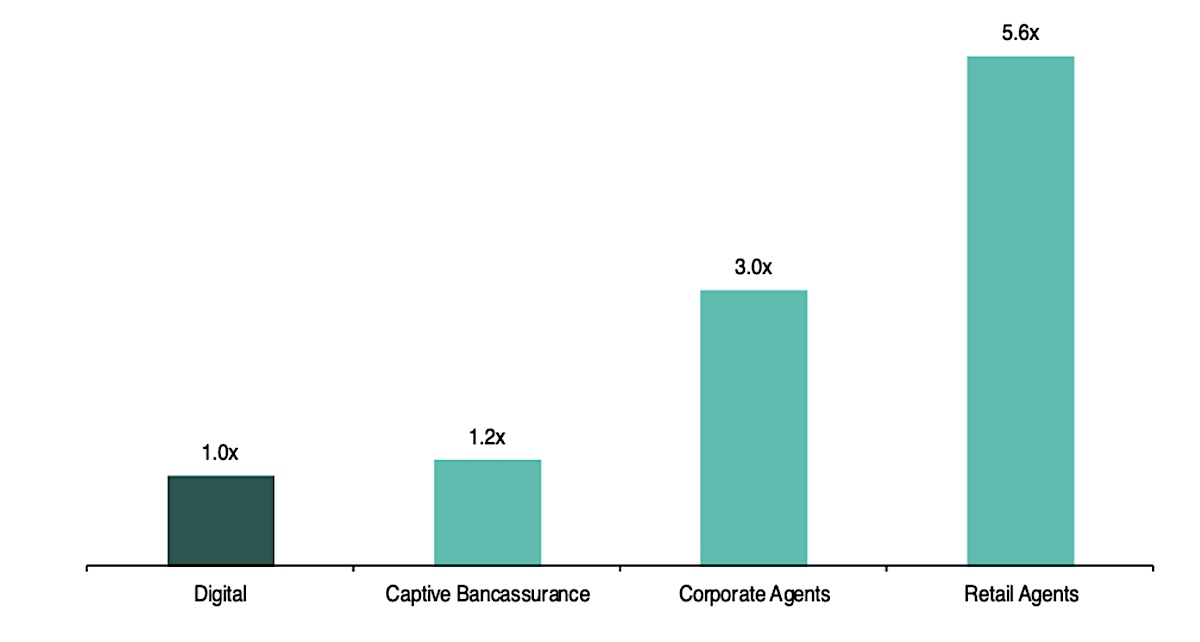

The startup has developed the insurance stack from scratch and partnered with insurers to include additional coverage on pre-existing conditions and dental, said Abhishek Poddar, co-founder and chief executive of Plum, in an interview with TechCrunch. (Like fintech firms, which partner with banks and NBFCs to provide credit to customers, online insurance startups maintain partnerships with insurers to provide health insurance coverage. Plum maintains partnerships with ICICI Lombard, Care Health, Star Health and New India Assurance.) Poddar, who has worked at Google and McKinsey, said Plum is making it increasingly affordable and enticing for businesses to choose the startup as their partner. Most insurance firms and online aggregators in India today currently serve consumers. There are very few players that engage with businesses. Even among those that do, they tend to be costlier and not as flexible. Plum offers its partnered client’s employees the option to top up their health insurance coverage or extend it to additional members of the family. Unlike its competitors that require all the premium to be paid annually, Plum gives its clients the ability to pay each month. And signing up an entire firm for Plum takes less than an hour. The speed is a key differentiator for Plum. Small businesses have to typically spend months in negotiating with other insurers. Bangalore-based Razorpay has also partnered with Plum to give the fintech startup's clients a three-click, one-minute option to sign up for insurance coverage.  Estimated cost of distribution for insurers across different channels in India (Bernstein, BCG) The startup plans to deploy the fresh capital to further expand its offerings, making its platform open to smaller businesses with teams as small as seven employees to sign up, said Poddar. The startup plans to cover 10 million people in India with insurance by 2025, and eventually expand to international markets, he said. India has an under-penetrated insurance market. Within the under-penetrated landscape, digital distribution through web-aggregators today accounts for just 1% of the industry, analysts at Bernstein wrote in a recent report. "As India's healthcare insurance industry rapidly expands and transforms, Plum is well positioned to make comprehensive health insurance accessible to millions of Indians. We are excited to partner with Abhishek, Saurabh and the Plum team as they scale their leading tech-enabled platform to employers across the country,” said Scott Shleifer, Partner at Tiger Global, in a statement. Plum is the latest investment from Tiger Global in India this year. The hedge fund, which has backed over 20 Indian unicorns, has emerged as the most prolific investor in Indian startups in recent months, winning founders with its pace of investment, check size and favorable terms. Last week, the firm invested in Indian social network Koo. |

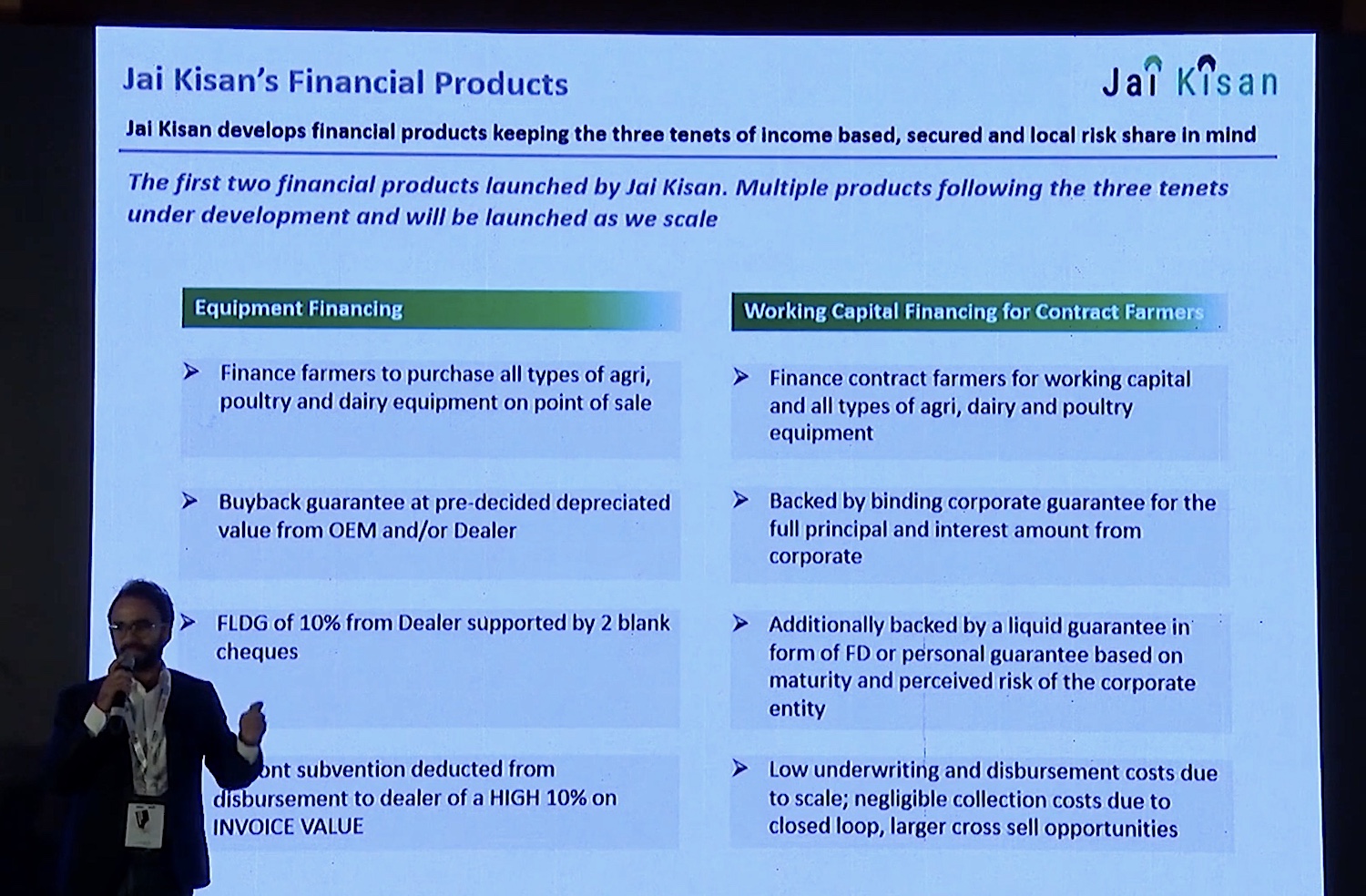

| Jai Kisan, a fintech startup aimed at rural India, raises $30 million Posted: 30 May 2021 06:31 PM PDT Jai Kisan, an Indian startup that is attempting to bring financial services to rural India, where commercial banks have a single-digit penetration, said on Monday it has raised $30 million in a new financing round as it looks to scale its business. Hundreds of millions of people in India today live in rural areas. Most of them don’t have a credit score. The professions they work on — largely farming — aren’t considered a business by most lenders in India. These farmers and other professionals also don’t have a documented credit history, which puts them in a risky category for banks to grant them a loan. Much of the credit these people do raise ends up getting invested in unproductive usage, which leads to higher interest and default rates. Three-year-old Mumbai-headquartered Jai Kisan is attempting to address this by treating farmers and other similar professionals as businesses instead of consumers. The startup has developed its own system — which it calls Bharat Khata — that is helping individuals and businesses get access to cheaper financing and ensures that the money they raise is being used for agri-inputs and equipment and other income generating purposes and enablement of rural commerce transactions. Arjun Ahluwalia, co-founder and chief executive of Jai Kisan, said financial services is crucial for these individuals as their entire economy depends on it. “The ability to buy now and pay later is how most people shop for things in India. Credit is an expectation by the Indian customer — it’s not a value added service,” he told TechCrunch in an interview. “If there is availability of formal financing to customers, it’s not just customer who does well. The entire ecosystem that revolves around that customer benefits,” he said, pointing to the rise of Bajaj Finance, which has helped several businesses flourish in India by giving credit to customers at the time of purchase, and Xiaomi, India’s largest smartphone vendor, which sells a large number of its devices to customers on monthly instalment plans.  Ahluwalia at a conference in 2019 (India FinTech Forum) Bharat Khata service, which was launched in April last year, captured more than $380 million of annualized GTV run-rate across over 25,000 storefronts by the financial year that ended in March this year, the startup said. “Jai Kisan has financed over 15% of the transactions which portrays the monetizability and quality of commerce being captured. The ability to have visibility and virality of high-quality transactions has enabled Jai Kisan to scale business by over 50% in 3 months. The unprecedented growth trajectory stands testament to Jai Kisan's capabilities to deploy capital efficiently by focusing on core customer credit needs,” the startup said. The startup, which operates in eight Indian states in South India, is now looking to scale its presence across the country and also increase the headcount. On Monday, it said it had raised $30 million in a Series A round led by Mirae Asset, Syngenta Ventures, and existing investors Blume, Arkam Ventures, NABVENTURES, Prophetic Ventures and Better Capital. An unspecified amount of the financing was raised as debt from Blacksoil, Stride Ventures, and Trifecta Capital. “Jai Kisan is at the cusp of disrupting the rural financing industry and we're glad to be a part of their growth story. Jai Kisan's stellar growth, excellent asset quality and expanding footprint make them a highly differentiated player in the segment,” said Ashish Dave, chief executive of the India Venture Investments for the South Korean firm Mirae Asset. “Mirae Asset has always believed in backing companies which aim to become category leaders which is evident from our other investments and we believe Jai Kisan is on the journey of doing so for rural finance,” he added. Like most fintech startups, Jai Kisan has so far relied on its banking and other financial institutions to finance credit to businesses. The startup said it will now finance 20% of all loans by itself. Which is why it is also raising some money in debt in the new round. |

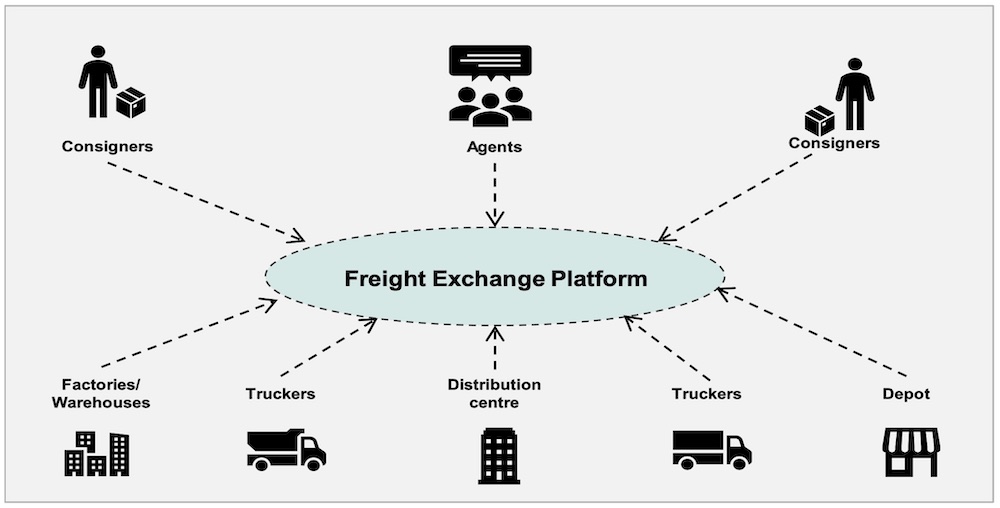

| Indian logistics giant Delhivery raises $277 million ahead of IPO Posted: 30 May 2021 10:29 AM PDT Delhivery, India's largest independent e-commerce logistics startup, has raised $277 million in what is expected to be the final funding round before the firm files for an IPO later this year. In a regulatory filing, the Gurgaon-headquartered startup disclosed it had raised $277 million in a round led by Boston-headquartered investment firm Fidelity. Singapore's sovereign wealth fund GIC, Abu Dhabi's Chimera, and UK’s Baillie Gifford also participated in the new round, a name* of which the startup didn’t specify. The new round valued the 10-year-old startup at about $3 billion. Delhivery — which also counts SoftBank Vision Fund, Tiger Global Management, Times Internet, The Carlyle Group, and Steadview Capital among its investors — has raised about $1.23 billion to date. Delhivery began its life as a food delivery firm, but has since shifted to a full suite of logistics services in over 2,300 Indian cities and more than 17,500 zip codes. It is among a handful of startups attempting to digitize the demand and supply system of the logistics market through a freight exchange platform.  Research and image: Bernstein Its platform connects consigners, agents and truckers offering road transport solutions. The startup says the platform reduces the role of brokers, makes some of its assets such as trucking — the most popular transportation mode for Delhivery — more efficient, and ensures round the clock operations. This digitization is crucial to address the inefficiencies in the Indian logistics industry that has long stunted the national economy. Poor planning and forecasting of demand and supply increases the carrying costs, theft, damages, and delays, analysts at Bernstein wrote in a report last month about India's logistics market. Delhivery, which says it has delivered over 1 billion orders, works with "all of India's largest e-commerce companies and leading enterprises," according to its website, where it also says the startup has worked with over 10,000 customers. For the last leg of the delivery, its couriers are assigned an area that never exceeds 2 sq km, allowing them to make several delivery runs a day to save time. Indian logistics market's TAM (total addressable market) is over $200 billion, Bernstein analysts said. The startup said late last year that it was planning to invest over $40 million within two years to expand and increase its fleet size to meet the growing demand of orders as more people shop online amid the pandemic. (*Indian news outlet Entrackr, which first reported on the filing, suggested it’s a Series H round. But according to insight platform Tracxn, there is no record of a Series G round for Delhivery. The startup didn’t comment on Sunday.) |

| For startups, trustworthy security means going above and beyond compliance standards Posted: 30 May 2021 08:08 AM PDT When it comes to meeting compliance standards, many startups are dominating the alphabet. From GDPR and CCPA to SOC 2, ISO27001, PCI DSS and HIPAA, companies have been charging toward meeting the compliance standards required to operate their businesses. Today, every healthcare founder knows their product must meet HIPAA compliance, and any company working in the consumer space would be well aware of GDPR, for example. But a mistake many high-growth companies make is that they treat compliance as a catchall phrase that includes security. Thinking this could be an expensive and painful error. In reality, compliance means that a company meets a minimum set of controls. Security, on the other hand, encompasses a broad range of best practices and software that help address risks associated with the company's operations. It makes sense that startups want to tackle compliance first. Being compliant plays a big role in any company's geographical expansion to regulated markets and in its penetration to new industries like finance or healthcare. So in many ways, achieving compliance is a part of a startup's go-to-market kit. And indeed, enterprise buyers expect startups to check the compliance box before signing on as their customer, so startups are rightfully aligning around their buyers' expectations.

One of the best ways startups can begin tackling security is with an early security hire. With all of this in mind, it's not surprising that we've witnessed a trend where startups achieve compliance from the very early days and often prioritize this motion over developing an exciting feature or launching a new campaign to bring in leads, for instance. Compliance is an important milestone for a young company and one that moves the cybersecurity industry forward. It forces startup founders to put security hats on and think about protecting their company, as well as their customers. At the same time, compliance provides comfort to the enterprise buyer's legal and security teams when engaging with emerging vendors. So why is compliance alone not enough? First, compliance doesn't mean security (although it is a step in the right direction). It is more often than not that young companies are compliant while being vulnerable in their security posture. What does it look like? For example, a software company may have met SOC 2 standards that require all employees to install endpoint protection on their devices, but it may not have a way to enforce employees to actually activate and update the software. Furthermore, the company may lack a centrally managed tool for monitoring and reporting to see if any endpoint breaches have occurred, where, to whom and why. And, finally, the company may not have the expertise to quickly respond to and fix a data breach or attack. Therefore, although compliance standards are met, several security flaws remain. The end result is that startups can suffer security breaches that end up costing them a bundle. For companies with under 500 employees, the average security breach costs an estimated $7.7 million, according to a study by IBM, not to mention the brand damage and lost trust from existing and potential customers. Second, an unforeseen danger for startups is that compliance can create a false sense of safety. Receiving a compliance certificate from objective auditors and renowned organizations could give the impression that the security front is covered. Once startups start gaining traction and signing upmarket customers, that sense of security grows, because if the startup managed to acquire security-minded customers from the F-500, being compliant must be enough for now and the startup is probably secure by association. When charging after enterprise deals, it's the buyer’s expectations that push startups to achieve SOC 2 or ISO27001 compliance to satisfy the enterprise security threshold. But in many cases, enterprise buyers don't ask sophisticated questions or go deeper into understanding the risk a vendor brings, so startups are never really called to task on their security systems. Third, compliance only deals with a defined set of knowns. It doesn't cover anything that is unknown and new since the last version of the regulatory requirements were written. For example, APIs are growing in use, but regulations and compliance standards have yet to catch up with the trend. So an e-commerce company must be PCI-DSS compliant to accept credit card payments, but it may also leverage multiple APIs that have weak authentication or business logic flaws. When the PCI standard was written, APIs weren't common, so they aren't included in the regulations, yet now most fintech companies rely heavily on them. So a merchant may be PCI-DSS compliant, but use nonsecure APIs, potentially exposing customers to credit card breaches. Startups are not to blame for the mix-up between compliance and security. It is difficult for any company to be both compliant and secure, and for startups with limited budget, time or security know-how, it's especially challenging. In a perfect world, startups would be both compliant and secure from the get-go; it's not realistic to expect early-stage companies to spend millions of dollars on bulletproofing their security infrastructure. But there are some things startups can do to become more secure. One of the best ways startups can begin tackling security is with an early security hire. This team member might seem like a "nice to have" that you could put off until the company reaches a major headcount or revenue milestone, but I would argue that a head of security is a key early hire because this person's job will be to focus entirely on analyzing threats and identifying, deploying and monitoring security practices. Additionally, startups would benefit from ensuring their technical teams are security-savvy and keep security top of mind when designing products and offerings. Another tactic startups can take to bolster their security is to deploy the right tools. The good news is that startups can do so without breaking the bank; there are many security companies offering open-source, free or relatively affordable versions of their solutions for emerging companies to use, including Snyk, Auth0, HashiCorp, CrowdStrike and Cloudflare. A full security rollout would include software and best practices for identity and access management, infrastructure, application development, resiliency and governance, but most startups are unlikely to have the time and budget necessary to deploy all pillars of a robust security infrastructure. Luckily, there are resources like Security 4 Startups that offer a free, open-source framework for startups to figure out what to do first. The guide helps founders identify and solve the most common and important security challenges at every stage, providing a list of entry-level solutions as a solid start to building a long-term security program. In addition, compliance automation tools can help with continuous monitoring to ensure these controls stay in place. For startups, compliance is critical for establishing trust with partners and customers. But if this trust is eroded after a security incident, it will be nearly impossible to regain it. Being secure, not only compliant, will help startups take trust to a whole other level and not only boost market momentum, but also make sure their products are here to stay. So instead of equating compliance with security, I suggest expanding the equation to consider that compliance and security equal trust. And trust equals business success and longevity. |

| You are subscribed to email updates from TechCrunch. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment