TechCrunch |

- Kuda, the African challenger bank, raises $55M at a $500M valuation

- Indian online insurer PolicyBazaar files for IPO, seeks to raise over $800 million

- Indian edtech Unacademy valued at $3.44 billion in $440 million fundraise

- Square to buy ‘buy now, pay later’ giant Afterpay in $29B deal

- Unicorns are ready for a haircut

| Kuda, the African challenger bank, raises $55M at a $500M valuation Posted: 02 Aug 2021 12:26 AM PDT Kuda Bank, the London-based, Nigerian-operating startup that is taking on incumbents in the country with a mobile-first, personalised and often cheaper set of banking services built on newer, API-based infrastructure, has been on a growth tear in the last several months, and to fuel its expansion, it has now raised another round of funding. TechCrunch has learned, and confirmed with Kuda, that the startup has closed, via its London entity, a Series B of $55 million — money that it plans to use to double down not just on new services for Nigeria, but to prepare its launch into more countries on the continent, and in the words of co-founder and CEO Babs Ogundeyi, to build a new take on banking services for “ever African on the planet.” The funding was made at a valuation of $500 million, and it comes on the back of some impressive early growth for the startup. “We've been doing a lot of resource deployment has been in our operational entity, in Nigeria. But now we are doubling down on expansion and the idea is to build a strong team for the expansion plans for Kuda,” Ogundeyi told TechCrunch in an interview. “We still see Nigeria as an important market and don't want to be distracted so don't want to disrupt those operations too much. It's a strong market and competitive. It's one that we feel we need to have a strong hold on. So this funding is to invest in expansion and have more experience in the company with relation to expansion.” Kuda now has 1.4 million registered users, which is more than double the number it had in March when it had 650,000 registered users — a figure it revealed when announcing its Series A of $25 million led by Valar Ventures. We understand that this latest Series B was a relatively quick inside round — that is, it’s coming from existing investors. Co-led by Valar Ventures and Target Global, it also includes SBI and a number of previous angels also participating. Kuda was not proactively raising money at the time the Series B was initiated and closed. “We felt that Babs and Musty” — Musty Mustapha, the co-founder and CTO — “are ambitious on another level. For them, it was always about building a pan-African bank, not just a Nigerian leader,” said Ricardo Schäfer, the partner at Target who led the round for the firm. “The prospect of banking over 1 billion people from day one really stood out for me at the beginning.” You might notice that it’s only been four months since Kuda last announced a round of funding. Equity rounds raised in quick succession, sometimes just months apart, seems to be the order of the day at the moment, fueled in part by a lot of money being pumped into venture at the moment, but also by the state of the market. When the company in question is showing all the right growth metrics and is working in a particularly buzzy area, many will strike when the iron is hot. (GoPuff, which last week confirmed a $1 billion raise just months after a previous round, is another example of that happening from a different corner of the world.) Neobanks — fintechs building a new generation disruptive of banking services based around more modern interfaces and infrastructure based around the concept of API-driven embedded finance — have been one of these areas, growing at a rate of nearly 50% annually in terms of revenues and projected to be collectively a $723 billion market by 2028. Within that, we’re seeing a number of strong players emerging across the globe built on this model — Nubank out of Brazil, Revolut and N26 in Europe, WeBank in China, Varo and Chime in the U.S. among them. In this regard, Africa may be the last great untapped region when it comes to banking, one reason why Kuda is being eyed up and is seeing strong adoption. The writing has been on the wall for years. A report from McKinsey on banking in Africa in 2018 identified a surge of interest in financial services that were delivered digitally, and that growth would be driven by a rapidly evolving middle class of consumers, while at the same time an ongoing death of accessible financial services for the majority of the population with some 300 million people still unbanked on the continent. It’s these three basic factors on which Kuda has built its own service. Kuda is not the only one building and raising and growing. Others raising money for new fintech plays include payments company Chipper Cash, Airtel Africa, online lender FairMoney and more. However, Kuda is unique among the neobanks in that it is building its services with its own banking license in hand. This means that it can be more flexible and fast-moving when it comes to creating new products or tweaking existing ones, and it gives the company another level of credibility in a region where those who were already banking with incumbents might be more wary of new players. Indeed, Kuda’s initial business model was built around providing banking services to people who still also held accounts with incumbent banks: people would have their salaries paid into their old accounts, and then transferred out to be spent and used in other ways via their Kuda accounts. Ogundeyi said that this is gradually shifting and more people are now bringing both paying-in and paying-out to their Kuda accounts. Ogundeyi would not say which countries would be Kuda’s next targets. But he did note that its most recently-launched product, Kuda’s first move into credit by way of an overdraft allowance, is a sign of the things to come. “It's a unique product, an overdraft that we pre-qualify the most active users for,” he said. In Q2 it qualified over 200,000 users and pushed out $20 million worth of credit. With a 30-day repayment, he said, so far default has been “minimal” because of the company’s approach. “We use all the data we have for a customer and allocate the overdraft proportion based on the customer’s activities, aiming for it not to be a burden to repay,” he added. Andrew McCormack, a general partner at Valar Ventures who co-founded the firm with Peter Thiel and James Fitzgerald, said that the still-nascent potential of the market, and how Kuda is approaching that, were behind its decision invest in the startup another time. "Kuda is our first investment in Africa and our initial confidence in the team has been upheld by its rapid growth in the past four months,” he said. “With a youthful population eager to adopt digital financial services in the region, we believe that Kuda's transformative effect on banking will scale across Africa and we're proud to continue supporting them." |

| Indian online insurer PolicyBazaar files for IPO, seeks to raise over $800 million Posted: 01 Aug 2021 09:45 PM PDT Indian online insurance aggregator PolicyBazaar has filed for an initial public offering in which it is seeking to raise $809 million, becoming the fourth startup in the past two months from the South Asian market to explore public markets. In papers submitted to the market regulator in India, PolicyBazaar said it is looking to raise $504 million by issuing new shares while the rest will be driven by sale of shares by existing investors. The 12-year-old startup — backed by SoftBank, Falcon Edge Capital, Tiger Global, and InfoEdge — said it may consider raising about $100 million in a pre-IPO round. Softbank plans to sell shares worth over $250 million, while PolicyBazaar founders are looking to sell shares worth $52.7 million, they said in the papers. PolicyBazaar serves as an aggregator that allows users to compare and buy policies — across categories including life, health, travel, auto and property — from dozens of insurers on its website without having to go through conventional agents. It operates in India as well as the Middle East.  PolicyBazaar website In India only a fraction of the nation's 1.3 billion people currently have access to insurance and some analysts say that digital firms could prove crucial in bringing these services to the masses. According to rating agency ICRA, insurance products had reached less than 3% of the population as of 2017. An average Indian makes about $2,100 in a year, according to World Bank. ICRA estimated that of those Indians who had purchased an insurance product, they were spending less than $50 on it in 2017. “India's life insurance market is expected to grow at 18.8% p.a. to reach ₹ 31.9 trillion (US$ 425 billion) in FY2030, driven by favorable macro indicators, rising awareness towards financial products and services, digitization and simplification of products and processes, online channels for distributions, innovations and customizations in products and favorable government policies and regulatory push,” the startup said in the papers. In a report early this year, analysts at Bernstein estimated that PolicyBazaar commands 90% of share in the online insurance distribution market. The platform, which competes with Acko as well as Amazon in India, also sells loans, credit cards and mutual funds. The startup says it sells over a million policies a month. "India has an under-penetrated insurance market. Within the under-penetrated landscape, digital distribution through web-aggregators like Policybazaar forms <1% of the industry. This offers a large headroom for growth," Bernstein analysts wrote to clients. Zomato, which had a stellar public debut last month, as well as fintech firms Paytm and MobiKwik have filed for their initial public offerings in recent weeks. |

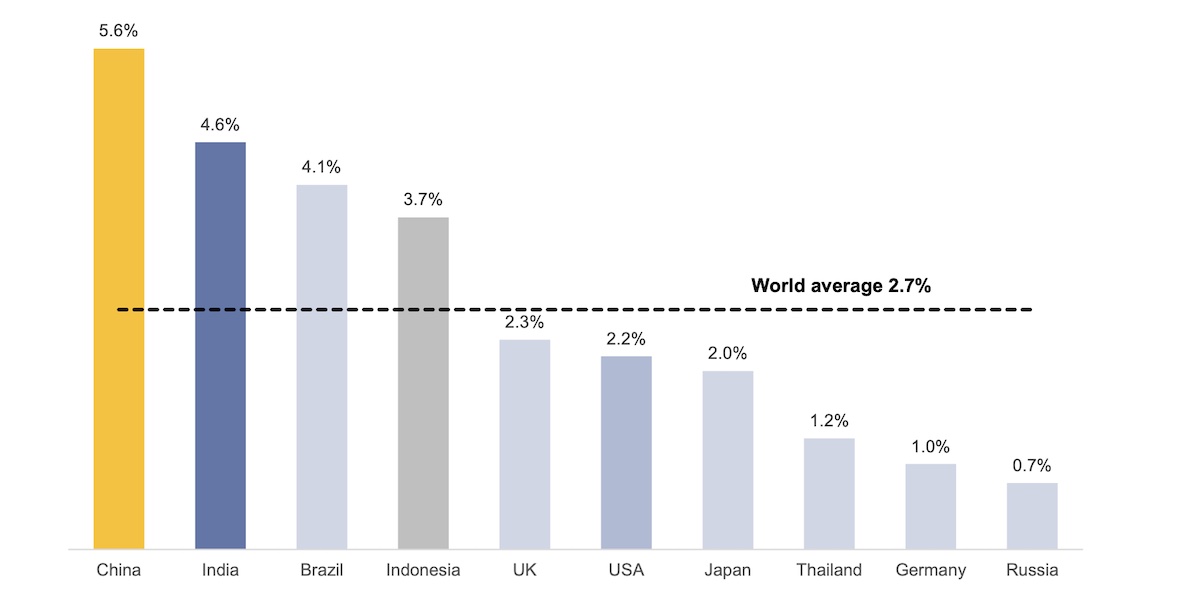

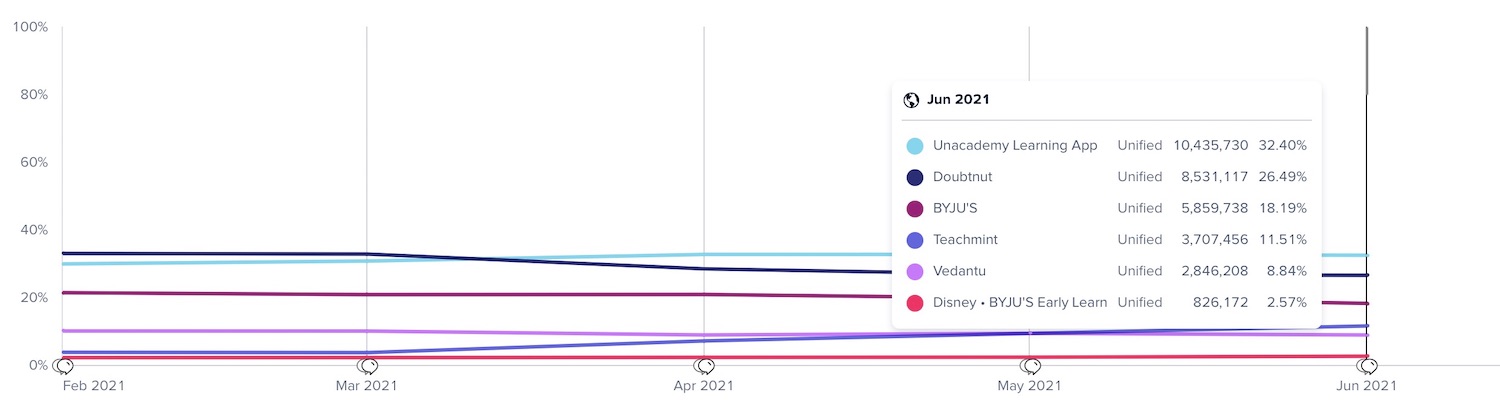

| Indian edtech Unacademy valued at $3.44 billion in $440 million fundraise Posted: 01 Aug 2021 06:15 PM PDT Indian online learning platform Unacademy has raised $440 million in a new financing round as investors double down on the South Asian market and elsewhere following a widening series of regulatory crackdowns in China that wiped hundreds of billions of dollars last month. Temasek led the Bangalore-based startup's new financing round — Series H — while Mirae Asset and existing investors including SoftBank Vision Fund 2, General Atlantic, Tiger Global as well as Deepinder Goyal of Zomato and Oyo’s Ritesh Agarwal participated in it, said the startup. The new round values the six-year-old startup at $3.44 billion, up from $2 billion in November last year. The investment brings Unacademy's to-date raise to about $860 million. The online learning platform, which began its journey on YouTube and still uses Google’s video platform to on-board educators, helps students prepare for competitive exams to get into college, as well as those who are pursuing graduate-level courses. On its app, students watch live classes from educators and later engage in sessions to review topics in more detail. The startup has over 50,000 educators on its platform, many of whom are very popular on YouTube. These educators help Unacademy sell more subscriptions and in return get a commission, according to industry executives familiar with the business arrangement. Unacademy has amassed over 6 million monthly active users (over 600,000 of whom pay for the service) in over 10,000 cities in India. Gaurav Munjal, Unacademy co-founder and chief executive, said the startup will deploy the fresh capital to broaden its bets on new categories such as upskilling, jobs and hiring. Relevel is “giving people a path to get their dream job irrespective of their educational background, while Graphy is “empowering creators to build their online businesses to sell digital goods including NFTs,” he said in a tweet. In a recent conversation with TechCrunch, Munjal said he wants Unacademy to become a consumer internet tech giant — perhaps the “Tencent of India.”  Spendings on education in India is among the highest globally (Source: A report from analysts at Goldman Sachs to clients last year.) The startup competes with scores of firms including Byju’s, which is India’s most valuable startup (at $16.5 billion valuation), TAL-backed Vedantu, Tiger Global-backed Classplus, and Lightspeed Venture-backed Teachmint. (TAL’s American depositary receipts have dropped to some 70% in recent days from $90 early this year as investors retreat following China’s crackdowns.) All these startups have reported growth in the past year as India — like most other countries — enforced lockdowns and closed schools to contain the spread of the coronavirus.  Monthly active users of education learning firms’ Android apps in India, according to mobile insight platform App Annie (sourced by TechCrunch from industry execs.) At stake is India’s online education market, which is estimated to generate $5 billion in revenue by 2025 (up from about $1 billion last year), according to analysts at Goldman Sachs. As of last year, there were about 6 million students in India who were paying for an online learning app, a figure Bernstein analysts expect to reach about 70 million by the end of the decade. Unacademy said last week it was creating a $40 million fund for educators on its platform. “On Day One (which is today) we already have more than 300 Educators eligible for the Grant which they will get immediately. Over the next few years we will give Grants of over $40M to our Educators,” said Munjal in a tweet. The new investment comes at a time when Indian startups are raising record capital and a handful of mature firms are beginning to explore the public markets. Business-to-business commerce and financing startup Ofbusiness said over the weekend it had raised $160 million in a new financing round (led by SoftBank Vision Fund 2) at a valuation of $1.5 billion, becoming the 18th Indian startup to attain the unicorn status, up from 11 last year. |

| Square to buy ‘buy now, pay later’ giant Afterpay in $29B deal Posted: 01 Aug 2021 05:12 PM PDT In a blockbuster deal that rocks the fintech world, Square announced today that it is acquiring Australian buy now, pay later giant Afterpay in a $29 billion all-stock deal. The purchase price is based on the closing price of Square common stock on July 30, which was $247.26. The transaction is expected to close in the first quarter of 2022, contingent upon certain closing conditions. It values Afterpay at more than 30% premium to its latest closing price of A$96.66. Square co-founder and CEO Jack Dorsey said in a statement that the two fintech behemoths "have a shared purpose." "We built our business to make the financial system more fair, accessible, and inclusive, and Afterpay has built a trusted brand aligned with those principles," he said in the statement. "Together, we can better connect our Cash App and Seller ecosystems to deliver even more compelling products and services for merchants and consumers, putting the power back in their hands." The combination of the two companies would create a payments giant unlike any other. Over the past 18 months, the buy now, pay later space has essentially exploded, appealing especially to younger generations drawn to the idea of not using credit cards or paying interest and instead opting for the installment loans, which have become ubiquitous online and in retail stores. As of June 30, Afterpay served more than 16 million consumers and nearly 100,000 merchants globally, including major retailers across industries such as fashion, homewares, beauty and sporting goods, among others. The addition of Afterpay, the companies' statement said, will "accelerate Square's strategic priorities" for its Seller and Cash App ecosystems. Square plans to integrate Afterpay into its existing Seller and Cash App business units, so that even "the smallest of merchants" can offer buy now, pay later at checkout. The integration will also give Afterpay consumers the ability to manage their installment payments directly in Cash App. Cash App customers will be able to find merchants and buy now, pay later (BNPL) offers directly within the app. Afterpay’s co-founders and co-CEOs Anthony Eisen and Nick Molnar will join Square upon closure of the deal and help lead Afterpay's respective merchant and consumer businesses. Square said it will appoint one Afterpay director to its board. Shareholders of Afterpay will get 0.375 shares of Square Class A stock for every share they own. This implies a price of about A$126.21 per share based on Square’s Friday close, according to the companies. Will there be more consolidation in the space? That remains to be seen, and Twitter is all certainly abuzz about what deals could be next. Here in the U.S., rival Affirm (founded by PayPal co-founder Max Levchin) went public earlier this year. On July 30, shares closed at $56.32, significantly lower than its opening price and 52-week-high of $146.90. Meanwhile, European competitor Klarna — which is growing rapidly in the U.S. — in June raised another $639 million at a staggering post-money valuation of $45.6 billion. No doubt the BNPL fight for the U.S. consumer is only heating up with this deal. |

| Unicorns are ready for a haircut Posted: 31 Jul 2021 11:00 AM PDT The digitization of your haircut may not have been on your 2020 bucket list, but 2021 has an even more surprising line item: Tech-powered barbershops are now a business proposition valued at nearly a billion dollars. Squire is a back-end barbershop management tool for independent businesses. I first covered it in the early months of the COVID-19 pandemic. The startup raised millions of dollars days before its key clientele — barber shops — were shut down across the country. The company eventually went from defense to offense in its growth strategy, finding itself as a key partner for any barbershop that needed to start offering contactless payments, digital appointment booking and a more seamless customer experience built for a generation used to doing everything online. This week, Squire tripled its valuation thanks to a Tiger-Global-led round. The company is now worth $750 million, after being valued at around $75 million when we first spoke to them. When I spoke to co-founder Dave Salvant, who launched the company with Songe LaRon in 2016, he explained how the company is now in a spot to expand into other barbershop-specific value propositions — either through acquisitions or partnerships. This week, for example, Squire announced that it launched a payment processing arm with Bond, a venture-backed fintech infrastructure company. The company also partnered with Gusto to bring on HR services for its clientele. Salvant noted how the progress of tech, especially financial services, lets them offer up a strong product without needing to build everything in-house. While these are partnerships for now, I wouldn't be surprised if we see Squire begin to scoop up companies that can unlock value from its existing datasets of how barbershops function and what kind of capital comes in and out of those doors. Behind the numbers:

It's a company to watch that fits into the narrative of pandemic rocked, then proven startups looking to expand with fresh capitalization. Less common, though, is that Squire is now en route to becoming a historical and unfortunately still rare Black-led unicorn. More data points, the better. In the rest of this newsletter, we'll discuss Robinhood's public debut and why a CEO thinks everyone needs to be them for a day. You can find me on Twitter @nmasc_. Robinhood sells Robinhood Image Credits: TechCrunch The long-awaited Robinhood IPO is no longer long-awaited. After pricing at the lower end of its range, the consumer investing and trading app's shares went down sharply, teetering between 8% to 10%. Here's what to know: IPO expert and fellow Equity co-host Alex Wilhelm gave us two reasons as to why Robinhood's stock went down. After all, we're used to pops in the consumer-facing tech company world.

Or maybe the company's warnings that its trading volumes could decline in Q2 2021 scared off some bulls. You get to be a CEO, you get to be a CEO! Image Credits: Richard Drury (opens in a new window) / Getty Images Now that free beer is no longer a company perk, the next best one may have emerged: Let anyone in your company become CEO for a day. Vincit CEO Ville Houttu implemented this program at his company in 2018 and said that the initiative has paid off "tenfold." Here's how it works, per the company:

You can see the resulting policies in our story, but in my humble opinion, the end result is definitely better than free beer. Around TC

Across the weekSeen on TechCrunch

For more public market news, subscribe to The Exchange by Alex Wilhelm and Anna Heim. Seen on Extra Crunch

Talk soon, |

| You are subscribed to email updates from TechCrunch. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment