StartupNation |

- Through Mentoring, Angel Investors Offer More Than Just Money

- Contemporary Cash Flow Management Tips for Startups

- Starting a Business? You Need to Research Your Number One Asset

- When Disaster Strikes, You Can Count on Dell

- WJR Business Beat: Marquette Is a Michigan Tech and Startup Hub (Episode 426)

- 7 Steps to Getting the Best Price When Selling Your Business

- Why I Would Rather Be Guided than Driven

- This Angel Investor Shares 11 Tips for Entrepreneurs to Raise Smart Money

- The Future of Gigging: Could the Gig Economy Save the Startup Market?

- 5 Top Tips to Galvanize Small Business Growth

- What About Mike? How to Handle a Weak Link on Your Payroll

- RJ King of DBusiness on Promising Detroit Developments

- WJR Business Beat: The Threat of Cybersecurity Breaches Can Devastate (Episode 425)

- The Role of Culture in a Remote Work Setting

- Eliminating Friction is Bad for Business. Embrace A Dose of Good Friction Instead.

| Through Mentoring, Angel Investors Offer More Than Just Money Posted: 17 Jun 2022 02:05 AM PDT

Captaining a new enterprise is like constructing a parachute after you've been thrown out of a plane: It's difficult, it's dangerous, you're pressed for time and a wrong decision can be fatal. When faced with the pressures of starting a new company, your ability to act quickly, decisively and correctly will depend on experience, skill and knowledge. If you are short on any of these attributes (not uncommon for the first-time entrepreneur), mentoring can make the difference between survival and doom. Mentoring is more than adviceTo be clear, a discussion of mentoring must distinguish between the expert, committed, hands-on and personalized guidance a good mentor provides and the mountains of generic, if well-meaning, advice available from a random assortment of friends, family, websites and newsletters. The adjectives associated with a good mentor include:

Related: How to Find the Right Business MentorInvestors as mentorsAngel investors are individuals and groups that fund promising startups. They are known as angels because they will often tread where venture capitalists (VC) and private equity firms fear to go—into the risky world of promising but unproven business ideas. They also frequently serve as mentors. That should be a win-win: You, as a budding entrepreneur, gain the benefit of experience and contacts, while the angels take positive action to help protect their investments. Angels serving as mentors are more likely to stay committed to your venture. The Angel Capital Association (ACA) is the world's largest angel professional development organization, with more than 13,000 investors in 260 angel groups and accredited platforms. The ACA membership has invested in more than 91,000 ventures. This is a good starting place to identify the angel investor groups in your region and investigate the opportunities for mentorship. Once a startup has grown to the point it needs additional rounds of funding, entrepreneurs will often turn to venture capital firms and private equity firms for financing. These firms frequently provide mentorship programs that are appropriate to your company's development stage. For example, New Enterprise Associates (NEA) is a large VC firm with mentorship programs for product design entrepreneurs. Specialized investors as mentorsYou might also be interested in mentorship programs from specialized angel investment groups and other sources. Some examples: Veterans:

Women:

Minorities:

6 Tips for Entrepreneurs to Successfully Pitch to Women Angel Investors |

| Contemporary Cash Flow Management Tips for Startups Posted: 16 Jun 2022 09:00 PM PDT

Running a startup can be difficult, especially regarding cash flow management. You need to ensure that you have enough business capital to cover your expenses, but you don’t want to tie up all your money in inventory or accounts receivable. The reality is that many startups fail due to poor cash flow management. To avoid becoming a statistic, you must be proactive about your cash flow. Here are some tips for contemporary cash flow management for startups, including invoice financing through a factoring company. Understand your cash flowAs a startup, one of the most important things you can do is keep track of your cash flow. This means understanding where your money is coming from and where it’s going. It’s essential to track your income and expenses regularly. This will help you see where your money is going and what areas you may need to cut back on. Working with a financial advisor who can help you understand your options and ensure you’re making the best decisions for your business is also essential. Take These 5 Steps to Establish Financial Well-Being as an Entrepreneur |

| Starting a Business? You Need to Research Your Number One Asset Posted: 16 Jun 2022 09:00 PM PDT

Your successful business model might take the form of a side hustle or full-time freelance work. Perhaps you've decided to invest in a franchise, or you've created an app for today's hot on-demand marketplace. There are lots of options, and no doubt you've given your choice of business and business model lots of thought. But how much thought have you given to the common denominator to all these entrepreneurial models? You! In launching your startup enterprise, you must examine the single most important factor in your eventual success or failure (yourself!) just as thoroughly you examine your options, opportunities and risks. I will go so far to say that your assessment of your own capabilities and limitations should be just as thorough as your evaluation of such business fundamentals as market demand, startup costs, access to financing, competitive landscape, etc.

Here's an example: Say you're an idea person but you have trouble implementing your great ideas. This self-knowledge will help you plan accordingly by compensating for this tendency, for instance, by partnering with someone with strong execution skills or working with a mentor or professional coach to focus on strengthening your own implementation skills. StartupNation exclusive discounts and savings on Dell products and accessories: Learn more here |

| When Disaster Strikes, You Can Count on Dell Posted: 16 Jun 2022 09:00 PM PDT For SMB to mid-market to the enterprise, agility is key. It's how you win in today's competitive environment. It's also why so many businesses are looking to the cloud for backup and recovery of business-critical data, workloads and systems. Cloud disaster recovery (DR) enables IT admins to back up data and applications to a secure off-premises location, providing off-site protection that enables virtual machines to quickly be brought up and running again in minutes in the case of a disaster – minimizing downtime and keeping business up and running. In fact, Dell EMC data protection reduces time to recover in the event of a disaster by up to 85%. TechBytes: Work From Anywhere But Make Sure It's Secure (Episode 2)For organizations that want to protect their VMware workloads, the Dell EMC Data Protection offering for VMware Cloud on AWS provides an extremely simple disaster recovery solution for workloads running on VMware Cloud on AWS. The DR solution, utilizing VMware Cloud on AWS, allows organizations to save VM images to Amazon S3 storage. Selected VM images can be recovered on demand to VMware Cloud on AWS in case of a disaster event, rather than recovering your entire VM environment at once. This solution offers business continuity, allowing you to continue operations in your own environment from a copy in VMware Cloud on AWS. This solution also requires Cloud DR Server running during on-going protection. Learn more about the benefits of cloud DR and how it works by clicking below:

StartupNation exclusive discounts and savings on Dell products and accessories: Learn more here |

| WJR Business Beat: Marquette Is a Michigan Tech and Startup Hub (Episode 426) Posted: 16 Jun 2022 07:29 AM PDT

On today’s Business Beat, Jeff talks with Joe Thiel of Innovate Marquette, who explains why Marquette, Michigan, is a hot spot in the tech and startup scene. Tune in below to learn more about Innovate Marquette:Tune in to News/Talk 760 AM WJR weekday mornings at 7:11 a.m. for the WJR Business Beat. Listeners outside of the Detroit area can listen live HERE. Are you an entrepreneur with a great story to share? If so, contact us at editor@startupnation.com and we'll feature you on an upcoming segment of the WJR Business Beat! Good morning, Paul! There’s a center of innovation emerging that is on the radar screens of those in the know with respect to the tech and startup space. But a deeper look makes clear why this is so. I had a chance to interview the CEO of Innovate Marquette SmartZone, Joe Thiel, who explained how and why the city of Marquette, Michigan, is now a hot spot in the tech and startup scene. The Innovate Marquette program was founded in 2015 as part of the Michigan Economic Development Corporation's focus on fostering entrepreneurship and business growth in the state. The cool thing about the Marquette program is that it covers the entire business continuum from idea to scale through its incubator accelerator combined program. Joe, first tell us about the incubator program. "So basically if you’re an entrepreneur, whether you’re a Main Street business, low technical tech cottage industry, high-tech scalable or product idea, we have all the resources in one building here to be able to satisfy your needs and get you through that process. "And the first phase of that really is identifying what the business is and what it does. So you have your mission, vision-centric considerations to your launch. You want to start doing some customer discovery early on and really identify what your MVP is going to be. Why is your business unique? Where do you fit in the marketplace, what your basic competition is and then can you protect your ideas." And then for those companies successful in getting past the incubator phase and then moving on to the accelerator program, Joe, tell us about that part of the program. "Once you make it into the accelerator, I’ve got my idea and I know what I want to do, and I know where I’m at in the market. Now I got to get everybody on board with me to scale it up and get out in the marketplace and generate revenue as fast as possible. Now, what’s my capital planning and what’s my partnership landscape look like, what’s my additional IP that I may be able to capture through partnerships, and then designing and developing the product, if it’s a product-based idea, to then be efficient enough to scale at some point." Sound cool? You bet it does. To learn more, go to: innovatemarquette.org. I’m Jeff Sloan, founder and CEO of startupnation.com, and that’s today’s Business Beat on the Great Voice of the Great Lakes, WJR. StartupNation exclusive discounts and savings on Dell products and accessories: Learn more hereThe post WJR Business Beat: Marquette Is a Michigan Tech and Startup Hub (Episode 426) appeared first on StartupNation. |

| 7 Steps to Getting the Best Price When Selling Your Business Posted: 16 Jun 2022 07:00 AM PDT

You may think that selling a business is just like selling a house: identify a buyer, support your price with comparable sales, fill out some paperwork, wire the funds and your deal is closed. Unfortunately, selling a business isn't quite that simple. A house is a tangible asset that's used for a very specific purpose: You live in it. A business, in contrast, is a complicated asset with tangible and intangible characteristics that are utilized to create future cash flow. Different assets require different processes. The mergers and acquisitions process is designed to attract multiple buyers, creating "deal heat" and competition that will drive the price and terms. This process works so well that it's been used for centuries by investment bankers around the world. However, if you don't understand and engage in this process properly, you risk the possibility of selling your business at a discount, with unfavorable terms or, worse, never selling your business. An Entrepreneur's Guide to Selling Your CompanyTo generate the highest price for your business, you'll want to follow this proven, seven-step process:

This process is complex, and issues will inevitably arise for both you and the buyer. But if done properly and with advisement, you can meet all of your objectives and enjoy the successful sale of your business. StartupNation exclusive discounts and savings on Dell products and accessories: Learn more here. |

| Why I Would Rather Be Guided than Driven Posted: 15 Jun 2022 09:00 PM PDT

The following is adapted from “Stop Chasing Squirrels: 6 Essentials to Find Your Purpose, Focus, and Flow“ by Ted Bradshaw. Copyright 2022 by Lioncrest Publishing. When I was a young businessman, chasing possibilities didn't seem like a bug of the system, but a feature. I was wide open, pedal to the floor, going after new business ideas and quickly shifting directions like a hockey player skating down the ice with the time about to expire. Which, by the way, was part of my identity back in the day. I was an entrepreneur. One of these directions, or maybe several of them, would hit pay dirt. It didn't particularly matter to me which of them did. That was my idea of what an entrepreneur is—someone who sees openings, grabs them, monetizes them, then moves on to the next big thing. But eventually, I came to a crisis point. I experienced a couple of panic attacks, seemingly out of nowhere. My inner life was in chaos, yet somehow I was the last to know—my body got the message to me through these two terrible experiences that felt like heart attacks. It was time to take stock of my life. Over time, and through facing up to certain hard truths for the first time, I came to realize I was a driven individual. The panic attacks were my body getting an urgent message through to my heart and soul: This path wasn't sustainable. It was killing me. I didn't want to be driven anymore. I did a lot of thinking about the right word, the one that described what I did want—and I came up with this one: guided. Here's why. The driven lifeIf you google the word "driven," you'll find a lot of information about the habits of highly motivated individuals. Being driven is generally presented as a positive thing, the description of those who have a high energy to get things done. Driven is one of those ambiguous words that can be used positively or negatively—like the word pride, for example. It's good to be proud of our children, or to take pride in our work. Yet pride is also listed as a sin! It's all about the nature of the pride, isn't it? Drivenness is similar. It's a positive or a negative depending on the driver. The problem comes in how and why a person might be motivated. Not every goal or source of emotional drive is a healthy one. Some driver is pushing us to our limits in order to get certain things done. It could be a sense of competition. Or it could be some need to prove ourselves, or live up to someone's expectations. Perhaps for a few minutes or a few days, it's possible to experience a sense of accomplishment. But then the driven person starts feeling that pressure again. Many driven people don't rest well. They don't care for their health as they should. Nor do they give enough thought to the people around them who are pulled along by this unrelenting course of rugged effort. Eventually, those with an unhealthy drive tend to burn out. They come to that point at which it's suddenly clear the goalposts are going to keep moving and the finish line will keep edging toward the horizon. Then something just cracks. They can't do it anymore. Being driven is letting the wind blow our boat every which way. It's being powered and directed by that merciless outside gust of wind. When we're driven, it feels, at first, as if we're going somewhere; we're on the move, maybe even fast. But the hidden truth is that you're not the one setting the direction. In the end, you end up way off course. Lost. Confused.

I asked myself how I like to be treated when I'm going places. There might be some meeting I need to go to, but I'm not too excited about it. You could get me there, I suppose, by threatening me. You could use a high-pressure sales approach. You could try frightening me into going, because of what I might miss. Maybe you'd be successful, but I don't really do well with that kind of pressure. I'd rather someone reason with me, tell me why the meeting's important, and give me good, solid encouragement that I should go because it's a very worthy meeting and I'll love what happens there. In other words, I don't want to be driven. I want to be guided. The guided lifeLet's go sailing. We talked about being driven by ill winds. The idea is that we're going somewhere, but we're being controlled by outside forces. That's being driven. Being guided is taking the initiative to bring a map—to adjust the sail and the rudder, to take up the oars, and to direct the vessel to a destination you've carefully chosen. Driven people tend to be unaware of the drivers. They're slaves to unknown masters. But guided people decide their own direction. And what guides them? A sense of purpose. It's possible, of course, to be guided by an unworthy purpose. You might be planning to rob a bank, and you might take a thoughtful, well-organized, efficient course toward a successful robbery. Obviously, that's not what we're describing. We all know there are healthy, worthy purposes. I believe everyone in the world has a purpose, and it's just the right fit for who we are—our talents, our temperaments, our values, and everything else about us. Finding and moving toward that ideal purpose is the surest formula for happiness and contentment. It's the exchange of my life and time for that which brings me the greatest joy and also makes the most positive difference in this world.

In my case, I found that I wasn't on that path. My purpose was not to create x number of new businesses or make y dollars in profit. It was not to build a kingdom dedicated to my sense of ambition. I know I've found my purpose for life. I'm guided by a deep and abiding passion for helping other people find their own unique purpose. It wasn't about me after all, in one sense, but about inspiring others. Yet ironically, because I've chosen this path and geared it to my gifts, it's actually a lot more about me than when I believed it was all about me. If that makes sense! The point is, I'm personally the happiest when I'm invested in the happiness of others. I know exactly what I want to do and how I want to do it, and each day is another mile in that direction. Goals? They're still there, but they look and feel different. My life is organized in a disciplined and orderly way around shorter- and longer-term goals that are thoughtfully based on my life focus. The journey beginsUnfortunately, you can't skip the parts of your life when the boat seems to be tossed about because that's where the journey really begins. You may be there right now. You have to face the "ill winds" that threaten to blow you off course. But there's also no reason to be discouraged. All of this is fuel. These tougher times are the ones that help us grow the most. I'd never be where I am now if I hadn't struggled through my own crises. I had to see what it was like and how it felt to lead a purposeless life. There is hope. Rest assured, you can find the purpose that will guide you if you're willing to seek it. For more advice on being guided, you can purchase “Stop Chasing Squirrels” on Amazon via StartupNation below. StartupNation exclusive discounts and savings on Dell products and accessories: Learn more here. |

| This Angel Investor Shares 11 Tips for Entrepreneurs to Raise Smart Money Posted: 15 Jun 2022 02:00 AM PDT

Often, I read articles offering tips for entrepreneurs that revolve around generic advice on getting started. However, what is often direly needed is how to appeal to investors and raise smart money — knowledge that is essential for fundraising and a master key to building, accelerating and scaling your new venture. The investment platform I founded and run, VenturePole, is the investment partner of HealthInc, the health tech accelerator of Startupbootcamp, the biggest startup accelerator organization in Europe. As part of my role as a partner of HealthInc, I sit on the jury for the startup competition in which 20 finalists pitch their ventures, with 10 then selected to enter the program. The winners receive support, including an investment, to accelerate and scale their ventures. In my additional role as a mentor, I help these startups get investment-ready in the program. LinkedIn co-founder Reid Hoffman once said, "Starting a company is like jumping off a cliff and assembling the plane on the way down." In my opinion, jumping off the cliff is the easy part; assembling the plane before you crash into a million pieces is what keeps founders up at night. As a founder and investor sitting on both sides of the table, I have consolidated my knowledge into the following tips for founders to raise smart money — funding from investors who can help you build your plane — which is one of the most beneficial things you can do for your company. StartupNation exclusive discounts and savings on Dell products and accessories: Learn more here |

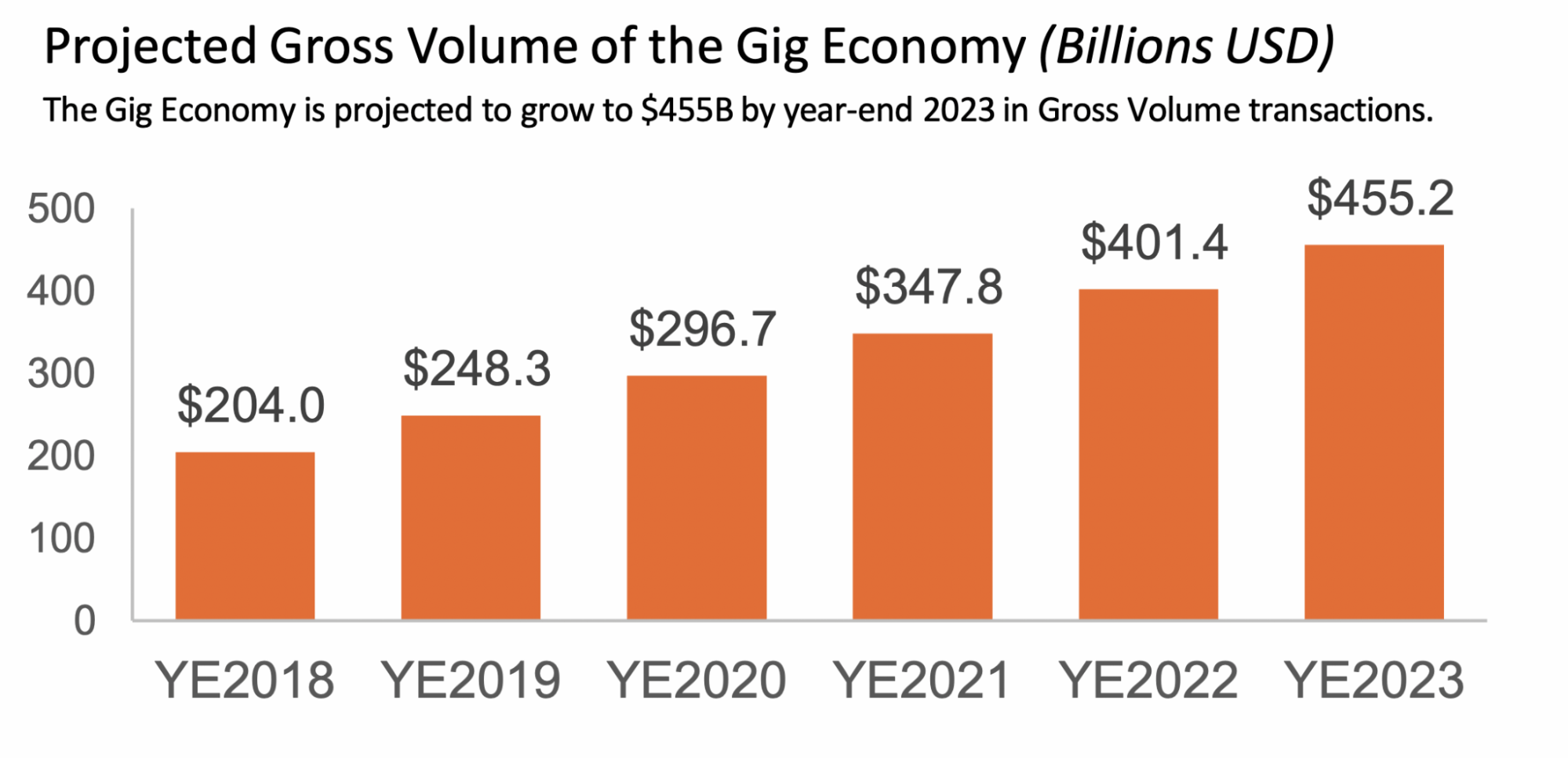

| The Future of Gigging: Could the Gig Economy Save the Startup Market? Posted: 14 Jun 2022 09:00 PM PDT The labor crisis has taken its toll on the startup market. After 47 million Americans quit their jobs in 2021, small business leaders are facing a national skill shortage. With more competition than ever before, the post-pandemic online playing field is ripe with rivals, yet stagnant with team players. While the e-commerce industry may have grown by a third in just two years, a global labor shortage is sure to put many entrepreneurial ventures out of business if company leaders don't act fast. Hiring Trends to Counteract Today's Staffing Challenges |

| 5 Top Tips to Galvanize Small Business Growth Posted: 14 Jun 2022 09:00 PM PDT

Economic and market instability over the last few years have left many small business owners stumped. What are the best strategies to not only survive this volatility but to thrive? Growing in a changing world requires an abundance of creativity, a willingness to try new ideas, and a sustained focus on the areas of business that will always matter. Incorporating growth strategies into your business as soon as possible will set your organization up for success in the long run. While the market may be unpredictable, your ability to take charge of your business' trajectory is not. Try out these strategies to get started this year. 1. Take your customers or clients seriously.As an expert in your field or in your business, it might sometimes feel like your customers or clients don't know what they want or how they want to receive it. This paradigm is shifting. Your potential customers are becoming savvier consumers every day. They have high expectations and if your business can't meet them, they'll head to the next business that can. That means you need to take their feedback seriously. Creating a genuine connection with your customer base means allowing them to participate in your company's story. Always strive to do better for your customers. Show your community that their opinions matter. Understand what they like and don't like about your products, services, or customer experience. Try out the changes that they want to see. You'll know from the response whether to keep going down that path or jump to another strategy. The Customer Is Always Right: Why Startups Should Pay Attention To CX Data |

| What About Mike? How to Handle a Weak Link on Your Payroll Posted: 14 Jun 2022 09:00 PM PDT

The following is an excerpt from "Who's Your Mike? A No-Bullshit Guide to the People You'll Meet on Your Entrepreneurial Journey" by Kurt Wilkin. Copyright 2022 by Per Capita Publishing. Do you have a Mike? He's been by your side from the beginning. He's been incredibly loyal – someone you could count on. But now you're facing your new hyper-growth reality—and you know he's going to make a ton of mistakes as he learns lessons the hard way—inevitably stunting your company's growth in the process. Do you move him into an individual contributor role and bring in a more experienced person to lead the team? Do you try and coach him up or make the hard choice to let him go? I bet this sounds familiar. I've seen some version of this play out with virtually every entrepreneurial client, friend, or peer I know. But I'm confident you have (or have had) one: someone who's been by your side for much of your journey, loyal and willing to do almost anything that's asked. They've been rewarded with promotions and responsibilities to the point where their titles are inflated and they're so far over their heads that they're at risk of imploding. And they're utterly exhausted. It's one thing to recognize you have a Mike and acknowledge that they're holding you and your company back. It's another thing altogether to take the hard steps to do something about it! As you scale your business, there are steps you need to take in order to professionalize it. One of the main things holding your Mike back is often one of the reasons he was so great early on. They're a bootstrapper who isn't afraid to roll up their sleeves. They won't ask their team to do anything they won't do. But that's the thing—they never built a team. They struggle with delegation and tend to do things themselves. Truth be told, this is a common struggle for many entrepreneurs, too! If you've promoted a Mike to a key role that he simply can't handle, something HAS to change. You're going to have to have some challenging conversations and you probably make some difficult decisions. But there's not one right answer. Every situation is different. In some cases, Mike may be willing to take a step back and admit this isn't working, or maybe he volunteers to leave for a leadership role with a smaller company. In some cases, Mike may be coachable and can either stay in his existing role and grow into it, or take a lesser role and acquiesce to a more experienced leader while he hopes to grow into a future leader (whether for your company or for a future employer). Unfortunately, sometimes Mike simply doesn't have a role going forward. He may be super important to you personally but has become a liability professionally. In the worst-case scenario, you lose your friend and former go-to guy because you just can't reconcile the needs of the business with the complicated emotions and egos at play. Again, Mike doesn't necessarily have to go. In fact, in many cases, Mike can be moved into an individual contributor role and leverage his work ethic and history with the company. With Mike, like most of the characters I discuss in the book, how you handle the situation often depends on their personalities, your relationship with them, and the work that needs to get done. The bottom line is that when you realize you have a Mike on your team, you're going to have to take action. Mike's in over his head, but you aren't—at least not yet. You don't have to sink with your legacy team! This is hard work. No one promised it wouldn't be. But if you really think about it, deep down in your heart, you're probably thinking about someone (or someones?) on your team right now. They're probably very well-intentioned and have been there for you in the past. But unfortunately, they're holding you and the company back. I like to shift the conversation from "What do we do with Mike?" to "What if we had a superstar instead of Mike?" Imagine you have someone in that role who has been where you want to go; someone who has previously doubled or tripled a company like yours; someone who has experience negotiating multimillion-dollar deals or scaling up operations or integrating multiple acquisitions. I don't necessarily mind learning lessons the hard way, at times. That's actually how I learn best. But it's pretty damn amazing to have someone on your team who has been through the battles, who has already learned those lessons, and has the scars to prove it. You want to leverage those lessons learned and get there faster, stronger and more efficiently. There's no reason why we need to learn all of these lessons the hard way. This entrepreneurial stuff is tough enough already! Challenging? Yes, but a necessary part of the process if you want to professionalize your team, scale your business, and take it to the proverbial next level. As my mom used to say, "If it were easy, everybody would do it." "Who’s Your Mike? A No-Bullsh*t Guide to the People You’ll Meet on Your Entrepreneurial Journey" can be purchased via StartupNation.com below. Sign Up: Receive the StartupNation newsletter!The post What About Mike? How to Handle a Weak Link on Your Payroll appeared first on StartupNation. |

| RJ King of DBusiness on Promising Detroit Developments Posted: 14 Jun 2022 08:14 AM PDT

Detroit has something other major cities in the world don't, DBusiness editor RJ King says on this episode of the “Inside Michigan Business” podcast: the ability to marry software with hardware. Tune in below:In this episode, RJ King talks with Jeff Sloan on topics such as:

For more, go to Inside Michigan Business. StartupNation exclusive discounts and savings on Dell products and accessories: Learn more here. |

| WJR Business Beat: The Threat of Cybersecurity Breaches Can Devastate (Episode 425) Posted: 14 Jun 2022 07:56 AM PDT

On today’s Business Beat, Jeff talks about cybersecurity threats and their impact on U.S. small businesses. Tune in below to hear the scary numbers:

Tune in to News/Talk 760 AM WJR weekday mornings at 7:11 a.m. for the WJR Business Beat. Listeners outside of the Detroit area can listen live HERE. Are you an entrepreneur with a great story to share? If so, contact us at editor@startupnation.com and we'll feature you on an upcoming segment of the WJR Business Beat! Good morning, Paul! Now, you know, it’s a killer for businesses these days, having to deal with cybersecurity issues. Isn’t there enough for entrepreneurs to have to worry about? Not only do small businesses have to focus on providing a solid line of defense against these threats, they now have to deal with added expenses relating to cybersecurity insurance. And boy, I’ll tell you, if you do get hit, Paul, it’s really time-consuming and costly to get things put back together, if you can at all. Because cybersecurity threats today can lead to catastrophic data breaches in which your business simply just can’t recover. Cybersecurity company Surf Shark just released findings compiled from an 18-year study and it suggests that the United States is the most data-breached country globally. The U.S. breached accounts make up 15.4% of all breaches. Since 2004, U.S. Internet users have lost an average of 27 pieces of data in online breaches. Now, as we know, the worst data breaches include the theft of passwords. Even more concerning, the bad guys have been effective at stealing passwords that are associated with names and contact information as well. This gives them broad access to do more harm than just what’s at their fingertips. Since the start of 2020, 2.2 billion accounts have been breached worldwide. Data shows that in the first quarter of 2022, 304 accounts were breached every single minute. Now there is some good news to report, even though the U.S. is the most data-breached country in the world, we are taking action to protect ourselves and as a result, the trend in the U.S. is that the breach rate actually fell by 33% in the first quarter of 2022 when compared with the same period a year ago. So look, if you’re a small business or frankly, even a big one, take action now to protect yourself and your company. This is for real. Make sure you have the proper technological defenses in place and get cybersecurity insurance on top of it. I’m Jeff Sloan, founder and CEO of startupnation.com, and that’s today’s Business Beat on the Great Voice of the Great Lakes, WJR. StartupNation exclusive discounts and savings on Dell products and accessories: Learn more here.The post WJR Business Beat: The Threat of Cybersecurity Breaches Can Devastate (Episode 425) appeared first on StartupNation. |

| The Role of Culture in a Remote Work Setting Posted: 13 Jun 2022 09:00 PM PDT

Having an almost entirely remote workforce is a relatively new concept for many business owners. People worked remotely before the pandemic, but COVID-19 lockdowns certainly introduced many more to the idea. Working from home is an excellent option for people with difficult commutes or health issues. However, startups may be finding it hard to establish workplace culture with hybrid and remote employees. Entrepreneurs need to develop a sense of community at work. It's even more critical when everyone's working from home. What are some ways startups can create company culture? Here are some reasons you need to do it and ways to get started. Why is company culture important?People working for a business want to feel like they're doing something important. One of the reasons you created your startup might have been for this exact reason. This is where company culture comes into play. Establishing ideals you would like to follow attracts people who share those thoughts. Once they're there, you have to encourage them to continue following through. Think about it — wouldn't you want to work for a company that values its employees and does what it set out to do? Without culture, the people who work for you will feel like they're just machine parts. Company culture lets employees know what they can expect from you. It includes how you go about business and ways you encourage workers. This can mean things like:

How you choose to treat those who work for you will make a big difference. Imagine working for a company with no goals and no interest in its employees. Maybe you've already been there and know how it felt. Good company culture will promote well-being and productivity. Research shows employee happiness can help businesses earn nearly 2% more and outperform their competitors. 5 Ways to Revamp Your Company's Culture |

| Eliminating Friction is Bad for Business. Embrace A Dose of Good Friction Instead. Posted: 13 Jun 2022 09:00 PM PDT

The following is an excerpt on leadership from "Friction: Adding Value by Making People Work for It," by Soon Yu and Dave Birss. Copyright 2022 by Zenkarma Media.

Employers and employees have seen the benefits of having a global workforce, both in terms of greater available pool of workers for employers, and more options of living anywhere. However, this has also led to employees having different expectations and greater optionality, resulting in the "Great Resignation." The remedy? Make work-life easier with even greater benefits. But these are just table stakes. Instead, consider making your employees work harder by adding good friction in their work lives. All friction is not created equal. There's bad friction, which should definitely be eliminated. And there's good friction, which creates more meaning, has a myriad of benefits, and should be protected like the rarest of employees.

Some things are worth fighting forThe frictionless approach is manifesting itself in even more ways. The current leadership approach is to make managing teams as effortless as possible. Many companies rely on software to remove effort and add trackable metrics. That might sound like a good thing, but it's leading to employers ignoring personal differences and treating everyone like an identical work unit. The corporate cookie-cutter slices off all the extracurricular activities and passions that make an employee attractive. And the value that these things could add is lost. You end up with a workforce of similar-minded, similar-thinking employees who struggle to think beyond the perceived limits of the organization. Conflicts are discouraged under the mistaken belief that they are bad for business. If any disputes arise, the HR department intervenes to ensure the offending behavior is nipped in the bud. This leads to a workforce that is too worried to disagree, speak up, or step on anyone else's toes. As a result, anything innovative or ground-breaking is self-censored before it has the opportunity to blossom. Maybe this all comes from a confusion between conflict and disrespect. From our experience, the best ideas come from respectful disagreement. But whatever the reason, this form of friction-elimination is unhealthy for business.

Instead healthy businesses encourage active disagreements to play out while creating a respectful and safe environment to harness the better outcomes from this interplay. The benefits of good frictionIt's commonly believed that depression leads to physical inactivity. But a study conducted by America's National Institute of Mental Health has shown that the correlation is the other way around. They discovered that people's physical activity affected their mood, whereas their mood didn't change their level of exercise. The less active someone is, the more chance they have of experiencing sadness. Humans are designed to be active — both physically and mentally. And the less active we become, the more it will manifest itself in our mental states. So less work doesn't always lead to healthier lives. Often good friction from purposeful work gives us the physical, social and mental stimulation we need to stay healthy. Without it, we don't function properly as human beings. The key for businessesAs employers and senior leaders paint bold visions and set higher goals for their companies and teams, employees should also have a hand in leading the charge. Give your employees more responsibility to increase belonging, engagement, and meaning. Task them with leading more strategic initiatives and have them present their ideas to larger audiences and in higher table stakes environments, while supporting them with resources and recognition. Encourage them to take on additional cross-functional leadership opportunities across the organization. Enlist employees to co-create an environment that fosters a stronger culture- whether it's participating in employee resource groups or planning a team building off-site. And don't forget to challenge their bosses to become better mentors for them and to champion them to stretch themselves. The key for businesses is to add “purposeful and rewarding” work to replace less meaningful tasks. "Friction" can be purchased via StartupNation.com below.

StartupNation exclusive discounts and savings on Dell products and accessories: Learn more here |

| You are subscribed to email updates from StartupNation. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment