Squared Away Blog |

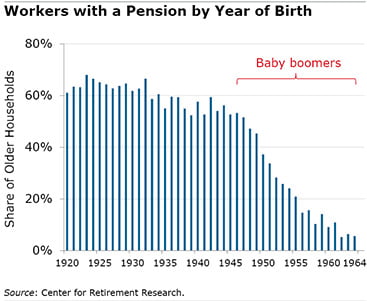

| Retirees with Pensions Slower to Spend 401k Posted: 24 Feb 2022 06:07 AM PST Retirees have long been reluctant to spend the money they've accumulated in their 401(k) savings plans. But it also used to be common for retirees to have a traditional pension to cover their regular expenses. By the time the baby boomers came along, pensions were available to a dwindling minority of workers, and it isn't entirely clear how much they'll tap into their 401(k)s.

Consider a simple example of the difference a pension makes. In the past, typical households that started retirement with a pension and $200,000 in 401(k)s and other financial assets had about $28,000 more at age 70 than their counterparts with $200,000 in assets but no pension. After age 75, the difference between the haves and have-nots widened to about $86,000. For this analysis, the researchers used data on the retirement finances provided in a survey of older Americans, specifically the heads of households born between 1924 and 1953, which includes some of the earliest boomers. The researchers also found that the pace at which these retirees spent their savings hinged on the percentage of wealth they held in the form of annuities, whether a pension, Social Security, or an insurance company annuity. The retirees who got more of their income from annuities depleted their savings more slowly. Based on prior generations' behavior, the researchers roughly estimated that boomers – given their lower pension coverage – are in danger of using up their financial assets at around age 85. This would leave them with little room in their budgets for a long life, a large unexpected medical bill, or an inheritance for their children. Boomers probably shouldn't assume then that their parents' retirement experiences are a reliable indication of how they will fare. To read this study, authored by Robert Siliciano and Gal Wettstein, see "Can the Drawdown Patterns of Earlier Cohorts Help Predict Boomers' Behavior?" The research reported herein was derived in whole or in part from research activities performed pursuant to a grant from the U.S. Social Security Administration (SSA) funded as part of the Retirement and Disability Research Consortium. The opinions and conclusions expressed are solely those of the authors and do not represent the opinions or policy of SSA, any agency of the federal government, or Boston College. Neither the United States Government nor any agency thereof, nor any of their employees, make any warranty, express or implied, or assumes any legal liability or responsibility for the accuracy, completeness, or usefulness of the contents of this report. Reference herein to any specific commercial product, process or service by trade name, trademark, manufacturer, or otherwise does not necessarily constitute or imply endorsement, recommendation or favoring by the United States Government or any agency thereof. |

A

A | You are subscribed to email updates from Squared Away Blog. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment